Stay on your retirement planning track and consider iBonds

Posted By RichC on June 25, 2022

It is stomach-churning to follow the often heard “hold tight” and “stick with the plan” advice often given by financial advisors. If you are currently retired and living off of a fix-income and nest egg, or are trying to prepare for retirement,  you are likely worried about times like these. Advisors tell you not to panic, and that with a properly allocated portfolio, markets will come back. Still, it is not easy to see 401-Ks and IRA portfolios shrink and years of savings disappear due to inflationary pressure in every area of the economy … especially the essential ones … like food, housing and energy.

you are likely worried about times like these. Advisors tell you not to panic, and that with a properly allocated portfolio, markets will come back. Still, it is not easy to see 401-Ks and IRA portfolios shrink and years of savings disappear due to inflationary pressure in every area of the economy … especially the essential ones … like food, housing and energy.  Each day the market sells off further, which can make ordinarily calm people search for a paper bag or act as if they are a nervous chipmunk. Perhaps that is why so many questions and articles are peppering the financial press these days?

Each day the market sells off further, which can make ordinarily calm people search for a paper bag or act as if they are a nervous chipmunk. Perhaps that is why so many questions and articles are peppering the financial press these days?

Just a cursory look at the ill-preparedness of today’s retirement population will either gives you a feeling that you are not alone … or hopefully … see yourself better prepared than others?

How many months of inflation, stagflation or a recession can we weather? According to a Senior Living article last month, “most retirees aren’t sitting on a nest egg the size of Fort Knox … median savings for ages 55-64 is just $104,000 and for those aged 65-74 it’s $148,000.” One can only hope most of them have equity in their house, some assets to sell, maybe a pension (teachers, government, military) or at least a solid social security check and a plan to keep expenses low (ie. live on less)?

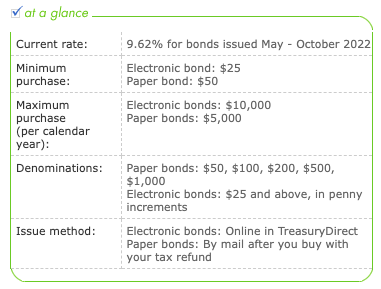

The point being is that some preparation is better than no preparation … and that if you are still working, focus on funding a diversified retirement savings portfolio. That means, don’t put all your eggs in one basket. A mix of investments that include growth and income, tech and consumer staples, energy and yes … even some bonds. We should all have some kind of emergency fund, normal savings and value accumulated in real estate (a home). If you’re ahead of the game, fund a 401K or IRA and maybe even some crypto, although if you don’t have money to lose … I’d avoid that last one. This year might be a good time to set up a Treasury Direct account and learn about iBonds (the yearly limit means starting younger and a contribution each year will give an account time to grow). Consider Series I Bonds as one more piece of your “saving for retirement” puzzle.

Comments