Using Home Equity as a bank or as a credit card?

Posted By RichC on August 26, 2016

Using the equity in a home isn’t anything new, but I’m old enough to remember when "we" first started to tap into home equity with Home Improvement Loans. "Back in the day" IRS deductions for interest on consumer credit (car loans, revolving credit, signature loans) were being phased out for all but home mortgages. Creative homeowners and bankers soon found ways around the loss of interest tax deductions and found that "improving ones home" added equity and could therefore be consider deductible on taxes. As the practice grew, as did the terms and the "collection of receipts for everything spent on a home" … even if the money from newly

Using the equity in a home isn’t anything new, but I’m old enough to remember when "we" first started to tap into home equity with Home Improvement Loans. "Back in the day" IRS deductions for interest on consumer credit (car loans, revolving credit, signature loans) were being phased out for all but home mortgages. Creative homeowners and bankers soon found ways around the loss of interest tax deductions and found that "improving ones home" added equity and could therefore be consider deductible on taxes. As the practice grew, as did the terms and the "collection of receipts for everything spent on a home" … even if the money from newly  accessed home equity from either a Home Equity Loan or HELOC was fungible.

accessed home equity from either a Home Equity Loan or HELOC was fungible.

Welcome to a loosening of tax policies and the renamed loan … now a Home Equity Line of Credit. Fewer restrictions and audits by the IRS gave homeowners readily accessible money at far more attractive rates than car loans, credit cards and signature loans. This became the boomers "bank" as they could continue to save for college and retirement while accessing cheap money utilizing they home as collateral. In the 1990s and 2000s many used the equity in their homes for "big purchases" … cars, college for their kids, wedding, etc. In the early years, few used HELOCs for general shopping or even vacations … and kept those items on month to month "plastic" credit cards. The banks felt secure in believing the lien on an "appreciating" home would protect them and this new financing was a great way to make money and keep customers happy … that was until it didn’t. (An aside: HELOC abuse is often cited as one cause of the subprime mortgage crisis.)

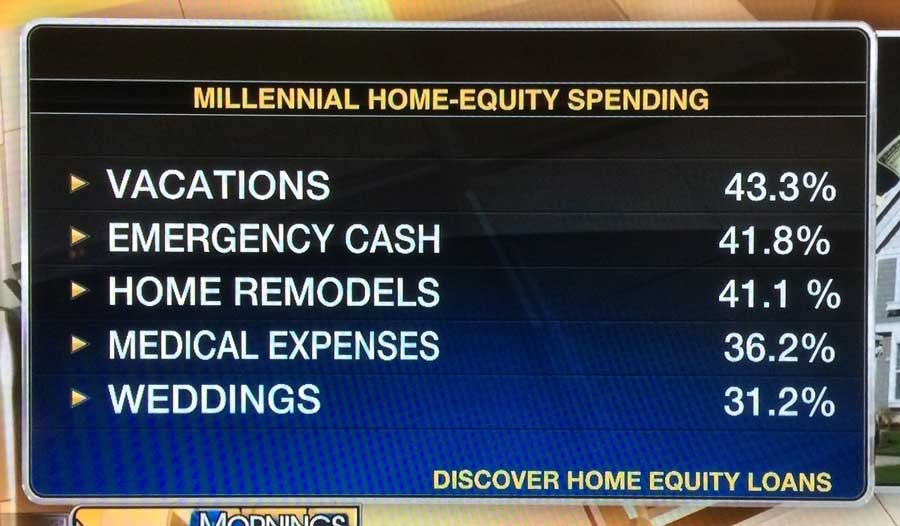

Home values collapsed and delinquencies rose as unemployment grew. Eventually leveraged homeowners couldn’t keep their homes nor pay their debts. We entered the worst recession since the great depression of the 1930s. Now, nearly a decade later, home values are rising again … and both banks and consumers are back at it again. Interestingly the millennial generation (first time home buyers) are following the footsteps of their parents and borrow against their newly acquired homes. But instead of using it as a "home improvement loan" … or even for a larger capital purchase  … some focus "experiencing life" or extravagant travel and vacations on credit. The home has now become the low interest credit card!

… some focus "experiencing life" or extravagant travel and vacations on credit. The home has now become the low interest credit card!

Some, including Dagen McDowell of Fox Business, argued that this is responsible money management and cheaper than putting it on a credit card. Others … the rest on the Mornings with Maria panel (above photo) … viewed it as "dangerous, irresponsible and the sort of borrowing that brought on the last housing crisis and recession." I chuckled when they began the "get off my lawn" jokes because it was "déjà vu all over again." It brought back memories of boomers being chastised by their parents for extending mortgages longer than 20 years or heaven forbid, borrowing more for home improvements rather than swiftly getting out of debt … let alone using the equity to pay for college or something as frivolous as wedding (cough, cough — guilty).

A clip that I thought was interesting was the discussion on a previous day about living within ones means … don’t spend more that you have and that it is important to save for retirement. Hard hitting (not unlike Dave Ramsey and his "rice and beans, beans and rice advice,") but critically important to be planning long term. Larry Winget was right, there are 40 years to save for retirement, but it all starts with living a lifestyle your income can afford — good advice for Washington DC too.

Comments