The retirement dividend income plan was challenged in 2020

Posted By RichC on February 17, 2021

For those of us living in a post-pension world, planning for retirement comes down to how much can be saved in 401K and IRAs …  and how to make it last once retired. Most people rely on the “multiple buckets approach” to coming up with enough dollars to pay for bills and “hopefully” live comfortably (Social Security, savings, real estate, reduced spending). Sadly, many will be falling short and relying on government, charity, family … and expecting to die early. It’s just the sad fact that even if we are saving, it is costing more to live. Taxes, utilities, medical care, autos, insurance, food and medicine continue to compete for our, savings. Even those who did everything right, might find that their self-planning or advisor’s advice is not working the way they had planned.

and how to make it last once retired. Most people rely on the “multiple buckets approach” to coming up with enough dollars to pay for bills and “hopefully” live comfortably (Social Security, savings, real estate, reduced spending). Sadly, many will be falling short and relying on government, charity, family … and expecting to die early. It’s just the sad fact that even if we are saving, it is costing more to live. Taxes, utilities, medical care, autos, insurance, food and medicine continue to compete for our, savings. Even those who did everything right, might find that their self-planning or advisor’s advice is not working the way they had planned.

Most advice, for those without a pension, goes like this:

Save in your tax advantaged retirement account ever year. Direct those dollars toward a balanced portfolio of primarily stocks, mutual funds or EFTs heavily skewed towards “growth” in your younger years and shifting towards more conservative “income” oriented and bonds in later years. The goal should be in growing your nest egg when time is on your side, then protect it without loosing value near …and in … retirement.

For many who grew up on slowly learning how equity investments work, sticking with what they know also makes sense. They (we) are most comfortable buying equities. The idea of balancing our portfolio with bonds, treasuries or CDs is difficult since yields barely keep up with CPI inflation and still have risk (and for seat of the pants economists, don’t keep up with “real” inflation – think health care costs, replacing cars or paying for home maintenance). What many see as US Dollar devaluation (think money printing, stimulus, deficits and debt) has everyone chasing a better return on their invested dollars. Conservative and aging investors are left pursuing stocks once again, which traditionally have the potential to grow and provide dividend income.

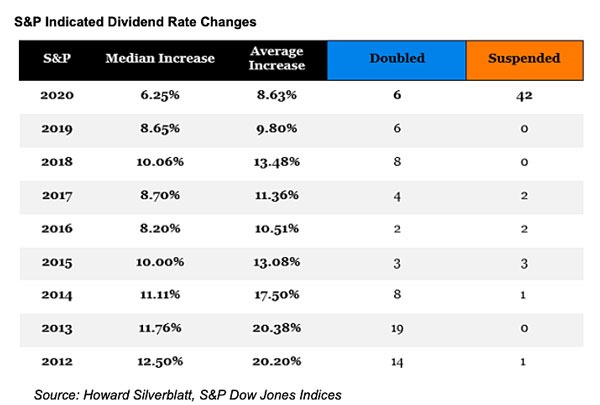

For many using this strategy, 2020 came as a shock. Dividends were suspended and even fewer companies could afford to increase their dividend payouts. This has a few struggling to decide on how to wisely proceed and prepare for 30+ years of income in their retirement. To paraphrase Robert Burns, “The best-laid plans of mice and men often go awry."

Comments