War, inflation, recession, oil prices and inverted yield curves

Posted By RichC on March 26, 2022

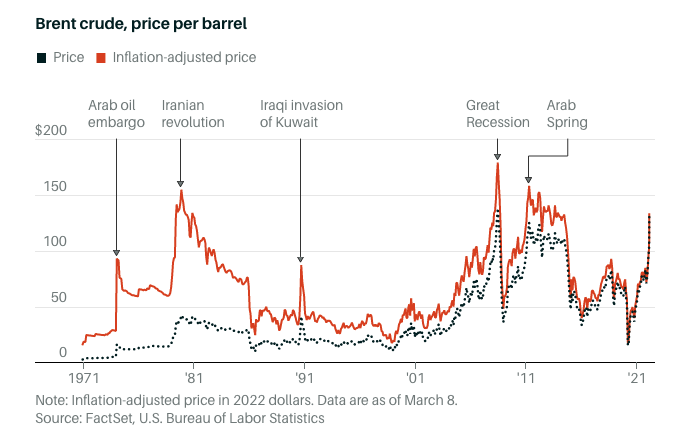

The “pain at the pump” is definitely real if you are buying fuel and if you have spend the last decade with gas and diesel at 40+% lower than we are seeing today. That said, in inflation-adjusted dollars, we are still off the highest per barrel prices that we have seen (chart below). Most oil traders expect the refined fuels at the pump to be even higher this summer before any additional capacity makes in “into the pipeline.”

Unfortunately that additional capacity, expected in 6 to 9 months, “could” come too late to prevent the next recession or the ability for most American to spend and keep the economy chugging along. If people stop buying, traveling, etc … people stop working and will have fewer dollars. If history teaches us anything, inflation is often brought into check by a recession or two. We can still hope that the Federal Reserve can manage a “soft landing” as they say and that perhaps the supply chain issues will ease some shortage pressure. BUT … now that Russia has invaded of Ukraine (major food supplier to Europe) we could see food shortages … and therefore higher prices … the next inflation kick.

Normally this is where I would add that the “lack of government discipline” (both DEMs and GOP) when it comes to borrowing and spending/wasting money, but I’ll refrain for now. Instead will point out an economic chart that points out Treasury yield curve inversions … a very accurate predictor of a recession, as mentioned before.

The Yield Curve Is Inverted! Remind Me Why I Care

If you’re wondering what a yield curve is and why there’s so much fretting in the U.S. over it flattening — and parts of it even inverting — you’re not alone. Late last year, Google searches for “yield curve inversion” shot up to their highest level ever. Here’s what the fuss is about.

1. What’s a yield curve?

It’s a way to show the difference in the compensation investors are getting for choosing to buy shorter- or longer-term debt. Most of the time, they demand more for locking away their money for longer periods, with the greater uncertainty that brings. So yield curves usually slope upward.

2. What are flat and inverted yield curves?

A yield curve goes flat when the premium, or spread, for longer-term bonds drops to zero — when, for example, the rate on 30-year bonds is no different than the rate on two-year notes. If the spread turns negative, the curve is considered “inverted.”

3. Why does it matter?

The yield curve has historically reflected the market’s sense of the economy, particularly about inflation. Investors who think inflation will increase will demand higher yields to offset its effect. Because inflation usually comes from strong economic growth, a sharply upward-sloping yield curve generally means that investors have rosy expectations. An inverted yield curve, by contrast, has been a reliable indicator of impending economic slumps, like the one that started about 11 years ago. In particular, the spread between three-month bills and 10-year Treasuries has inverted before each of the past seven recessions.

4. What’s been happening with U.S. yield curves?

The flattening trend that took the market by force at the end of 2017 continued through 2018, as the Federal Reserve continued to raise short term rates. But in March, the central bank policy makers lowered both their growth projections and their interest rate outlook, with the majority of officials now envisaging no hikes this year. That’s down from a median call of two at their December meeting. Concern about a possible economic slump and the prospect of the Fed having to cut short-term rates led the yield gap between 3-month and 10-year yields to vanish in a surge of buying that pushed long-term rates sharply lower.

The Reference Shelf

- A Federal Reserve Bank of San Francisco paper on the squeeze on the yield curve.

- Frequently asked questions on the yield curve from the Federal Reserve Bank of New York.

- A Federal Reserve Bank of Richmond paper wonders whether yield curves may now invert for reasons other than recession risks.

Comments