Stocks: ‘BUY’ trigger reached for RAD

Posted By RichC on July 26, 2007

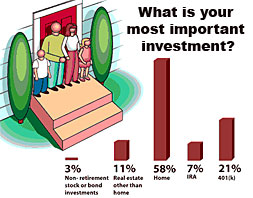

Those who know my daily routine see me nosing around in the stock market — sort of a hobby. Yes it is a relatively risky business, but if managed wisely one’s investments can mature at a significantly better rate than many ‘pay for’ advice organizations in selecting mutual funds, bonds, CDs, etc. Before talking ‘stocks, ‘ my first recommendation is to buy a home first. Younger readers should consider a home as an investment in your future — one that you can enjoy today. Traditionally homes are the best investments average Americans make in securing their future and the downside usually is minimal. Not only have most homes increased in value over a persons lifetime, but they offer a significant way to ‘use other people’s money’ (a home mortgage) in helping to finance and the buyer will receive an income tax deduction to boot. Another current tax boon for most home owners, that they don’t think about until later in life, is that the ‘capital gains’ exemption from the sale of their primary residence. This can significantly add dollars to their retirement porfolio. A home investment is hard to beat considering people need a roof over their heads anyway.

Those who know my daily routine see me nosing around in the stock market — sort of a hobby. Yes it is a relatively risky business, but if managed wisely one’s investments can mature at a significantly better rate than many ‘pay for’ advice organizations in selecting mutual funds, bonds, CDs, etc. Before talking ‘stocks, ‘ my first recommendation is to buy a home first. Younger readers should consider a home as an investment in your future — one that you can enjoy today. Traditionally homes are the best investments average Americans make in securing their future and the downside usually is minimal. Not only have most homes increased in value over a persons lifetime, but they offer a significant way to ‘use other people’s money’ (a home mortgage) in helping to finance and the buyer will receive an income tax deduction to boot. Another current tax boon for most home owners, that they don’t think about until later in life, is that the ‘capital gains’ exemption from the sale of their primary residence. This can significantly add dollars to their retirement porfolio. A home investment is hard to beat considering people need a roof over their heads anyway.

The above is not really the purpose of this post since most people realized that home ownership is not enough to secure their future; we must also save elsewhere. That second savings vehicle should be a 401-K if it is available … its a no-brainer if your company offers to contribute too. Do what you can to maximize your companies contribution as this is your second best tax savings retirement vehicle. Unfortunately not all of use have this option and have to shift to SEP, Keogh or IRAs. Individual Retirement Accounts are something available to all that earn and income as a way to save for retirement. They are currently available in a couple popular ‘flavors:’ Roth and Traditional. The Roth is attractive as the money earned in the account is promised to be tax free when withdrawn. The traditional shelters dollars going in and growing, but taxes will have to be paid on the back end when you withdraw — often at a non-working rate if you are fully retired.

IRAs can be self managed or broker managed … suffice to say I appreciate the freedom of being in control of this choice (my many mistakes and all). Personally I believe in a conservative philosophy in directing these investments; balanced investing is the key. I recommend picking leading companies in each market sector, corporate and municipal bonds (or bond funds – my choice) and try to keep them there for the longer haul … at least for the ‘less’ risky component of your IRA. I also like a chunk of cash free to trade in and out of the market. Call it the calculated risk chunk of my IRA and non-IRA ‘cash’ trading account. This is the cash used to make trades that are not intended to be long haul investments, but are ones which statistically offer a good chance of returning market beating numbers.

Here’s a trade that I currently like: WhenRAD (Rite Aid) RSI drops and the stock price heads lower (selling pressure), there comes a point when buyers start to outnumber the sellers. When this selling trend reverses and becomes a buying trend, the stock price heads back up. In each case in the technical chart when the RSI indicated a significant oversold situation this past year, buyers were back and the stock price has risen. (and when this happens to a $5-$6 stock it doesn’t take as many dollars to participant and offset trading commission cost.)

What to do? If you are aggressive and can’t help but want the bottom … you’ll start buying now and adding to your position over the next several days. If you are conservative, you’ll wait for a reversal of the downtrend … my rule of thumb is to wait 3 days for ‘the trend’ before buying. That said, I’m not very patient and I generally can’t pick a bottom and almost always get out too soon settling for a ‘fair’ gain in a short trade (often just daily moves). BTW … I’ve kicked myself many times in buying and selling trendy stocks like — Crocs – CROX. (See post) WARNING: Their is always risk … the market might continue to tumble and defy the statistics, so set your risk tolerance. (mine is a 10% … if the signal is wrong and things continue to deteriorate then you must bail with a 10% loss realizing that its going to take 2 good trades to get you back into the positive again.)

Comments