With tax uncertainty, how do we plan for retirement?

Posted By RichC on February 22, 2012

The tax season is upon us and many take this opportunity to take account of our retirement strategy (at least those who are thinking ahead). Years ago … in the days of the company pension, confidence in Social Security and Medicare and the assumption that one would retire at 65 after a lifetime career with a single company not has much thought was required … but times have changed. The pension is gone, the Social Security and Medicare system stressed and a guaranteed mid-60s retirement a thing of the past. On a positive note, some of us are healthier and will live longer and a few white collar employees or entrepreneurs may be fortunate enough to be healthy enough to work longer. What has changed nowadays is that we need to be accountable for our own retirement planning and that’s a challenge.

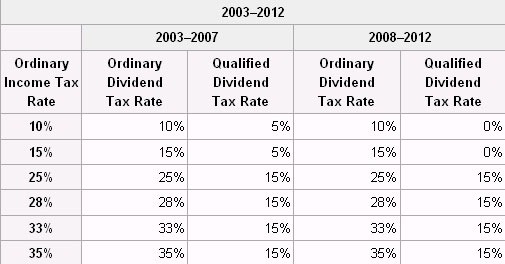

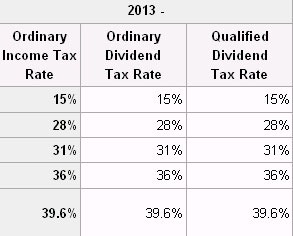

Current tax rates for those saving and planning for retirement around dividends

Not only are we faced with being responsible regarding the early saving for retirement in safe but growing investments that stay ahead of inflation, but also we need to navigate a challenging and changing tax code. From IRAs, Roth IRAs, 401Ks, Mutual Funds, ETF, corporate, government and treasury bonds, bank savings vehicles,  insurance products, stocks, real estate and trusts, we have complicated the process …which for many is like navigating a mine field; who has the tools or training to detect all of the hidden dangers? Add the federal governments tax code and future changes … and planning becomes a guessing game.

insurance products, stocks, real estate and trusts, we have complicated the process …which for many is like navigating a mine field; who has the tools or training to detect all of the hidden dangers? Add the federal governments tax code and future changes … and planning becomes a guessing game.

The recent hot potato item of taxing dividends is on the table for those currently retired or planning for it (possible increases for 2013 to the left). Now besides the “double taxation” associated with taxing a company’s income then re-taxing the distribution dividend to “owners,” the second tax also disproportionally impacts the savings and income seniors need to plan for retirement. If dividends are taxed at higher rates, this could discourage companies and their investors from long term investing … not to mention the income seniors are using to pay their cost of living expenses.

I understand that the government’s new goal is to tax the wealthiest Americans overall income (passive or earned) at higher rates and in turn increase the overall taxes they pay, but the targeting of twice taxed dividends at a time fewer and fewer retirees have other ways to save is a bad approach. I don’t love the Alternative Minimum Tax (AMT), but it make far more sense than raising taxes on dividends (personally I’d rather see a lower, but simplified tax – Steve Forbes tax postcard has always looked attractive to me).

Comments