Will we ever see modest interest rates again? #TBT

Posted By RichC on March 26, 2020

When I was growing up, I had a passbook savings account that was a teaching tool used by my parents to instill responsible money management. I deposited a small amount in it every few months or so when my mom would go to the bank and got my passbook stamped with an update as to what was in the account. I the early years, the update generally reflected my birthday money from my aunt, uncle and grandparents … plus interest compounded each month … almost always it seemed at a steady 5% rate. As I grew older, I began to earn money as a young entrepreneur who mowed lawns and collected/buried dead fish for a commercial fishery. The passbook savings account grew and I loved seeing the interest added each year … still 5%/year.

There were the few occasions that I dipped into my savings to make a major purchase (also part of the lesson), I never recall using all the money that was in the account. The two big purchases that I can recall:

There were the few occasions that I dipped into my savings to make a major purchase (also part of the lesson), I never recall using all the money that was in the account. The two big purchases that I can recall:

1) a ten-speed bike and

2) a 3.5 HP Eska outboard motor for my dinghy.

Both provided me years of service and I kept the dinghy and used it on our first boat Brenich!

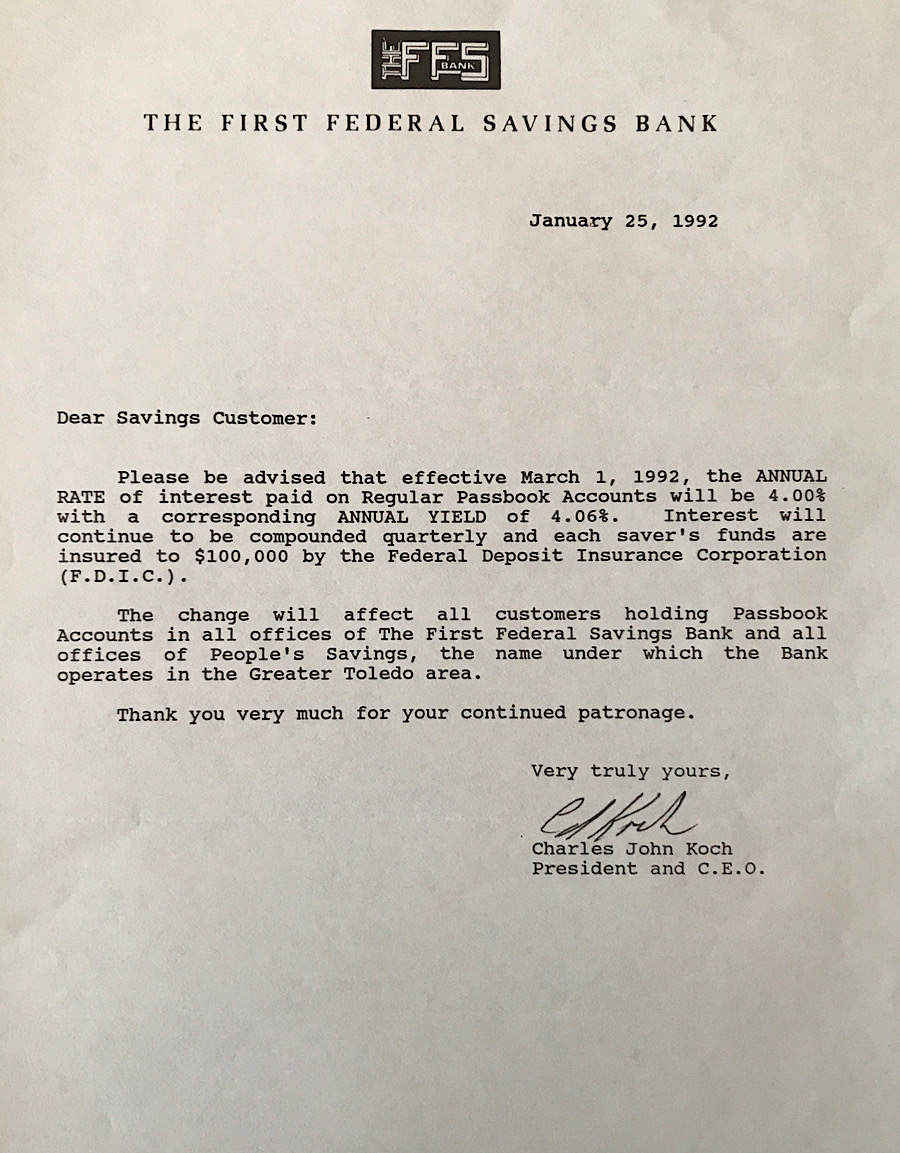

The point of this ThrowBack Thursday #TBT post, including a 1992 bank letter to Brenda and me regarding a “change” in interest rates on our savings, is that the only return on savings today comes with risk. Sure there was risk associated with bank savings accounts in the past, but it was that inflation could deflate the value of your savings plus interest (meaning inflation would need to exceed 5%/year). That seemed like a tolerable risk in the 1960s, but then came the late 1970s and 1980s (something we were well aware of when saving for and buying our first house in 1982 – we assumed a 12% interest mortgage when new mortgages were at 18%).

Then in the 1990s as a young business owner and father, saving again became critical as college costs and retirement savings became important to think about. I recall purchasing my first U.S. Treasury Bond and contemplating that “if I could ladder enough of these 9.75% bonds together over my lifetime that we could retire comfortable on the interest?” It was not to be for conservative returns (as can be seen with ALL pension plans). As rates continued to plummet, there was no way to generate a nest egg or save for college using any of the “safe” methods of saving money. The only returns possible was with a risk in the stock market or the variety of funds “spreading the risk” instead of investing in individual companies. Interest rate products were out as the few meager percent (if that) were almost a guaranteed way to lose buying power. I can’t imagine being in Europe where savers pay banks to hold their savings!

Where are we going? Well … with the latest 2.5 Trillion dollar infusion of money by the U.S. government to fight the Coronavirus caused economic crash, who knows? We are in uncharted territory, unless you can remember the 1930s. Perhaps the lesson to learn is that when we humans think we have things figured out, we likely don’t.

Comments