The economy: 5 Lessons From 1Q 2017 – Jim Glassman

Posted By RichC on May 20, 2017

Every once in a while comes an “it’s a small world“ surprise and one wonders, “why didn’t I know this?” This past week, my sister-in-law sent me a link to an article from her husband Dan Glassman’s brother Jim. The link was to Jim’s Linkedin page and opined on the economy. I figured … we are all amateur economists and doodle our opinions on blogs and social networks since everybody has access the Internet and self-publishing platforms nowadays — I figured I would check it out later.

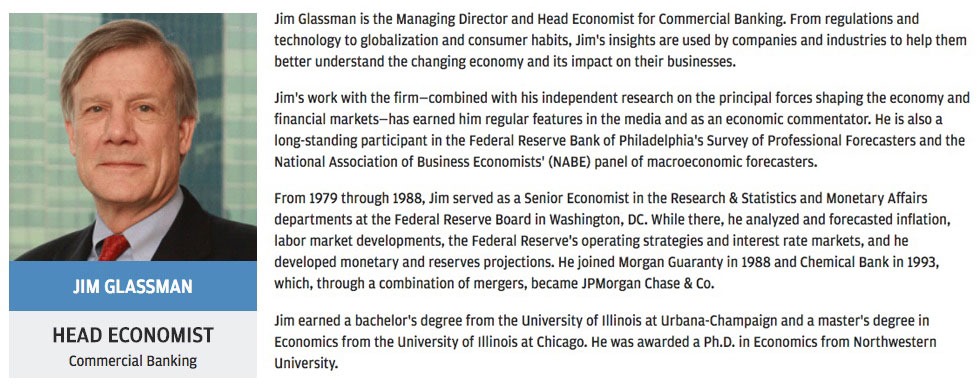

After finally reading, I found out Dan’s brother is Jim Glassman of JPMorganChase and his opinion as “head economist” is actually a bit more respected than those of us who run around bloviating on the subject; he actually gets paid for his opinion! Obviously a few “higher on the finance education chain” (JPMorganChase) think so too and have found his thoughts worthy of their attention.

Click above image for larger and to read Jim Glassman’s bio

After noting this, I read his latest article on “5 Lessons From the 1Q 2017” with a bit more interest and even search back to read a few more articles … and watched his presentations and TV interviews. Very impressive credentials and worthwhile thoughts. Thanks for sharing, Lynda!

Coming out of the first quarter, the focus may have been on GDP figures, but there are plenty of other lessons to learn from the first three months of 2017, including these five key takeaways.

The primary news coming out of the first quarter was the disappointing GDP figure, signaling US economic expansion slowed to a 0.7 percent annualized rate over the first three months. As discussed in last week’s article, there are broader measures that should also be considered when evaluating the economy’s health. This week, we focus on five key lessons coming out of 1Q.

1. We’re Not “Due” for a Recession

The recovery is wrapping up its eighth year, placing the current period of economic expansion among the longest on record. Fortunately, the business cycle doesn’t run on a calendar, and recessionary risks should remain low until the Federal Reserve fully normalizes interest rates.

Despite having taken the first steps toward normalization, the current monetary posture remains quite accommodative. Not only are short-term rates still at historically low levels, but the lingering effects of quantitative easing have also pushed long-term borrowing costs below their natural level. Artificially low borrowing costs should allow the economy to absorb imbalances that might otherwise lead to a recession.

2. Profit Slumps Don’t Tell the Full Story

Weak profits and falling corporate expenditures have often preceded recessions, but not every period of declining profitability has signaled a downturn. The decline in capital spending and corporate profits that accompanied the oil glut wasn’t a sign of weakness in the broader economy. While capital-intensive oil exploration projects were paused, consumers enjoyed the windfall from falling fuel prices. The resulting benefits from cheap oil are still materializing across the entire consumer sector, but the pain was immediately felt by energy companies and oil patch towns. However, the dislocations from falling oil prices will ultimately be overwhelmed by the benefits accompanying rising household wealth.

3. The Fed Focuses on the Big Picture

With the economy near full employment, the Fed is shifting its strategy toward prolonging the business cycle’s peak. After eight years of above-trend growth, the recovery’s health is no longer in doubt, and the Fed is likely to begin taking a more conceptual approach to interest rate normalization.

Over the coming year, monetary policy decisions will be guided by the long-term goal of withdrawing accommodation in a predictable fashion, even if that means being less responsive to the most recent economic data. Individual economic reports are always volatile, and the importance of monthly figures is likely to fade as the Fed’s focus shifts toward promoting long-term sustainable growth. Expect the Fed to stick to the plan, even in the face of temporary weakness.

4. Economic Activity Doesn’t Stop for Uncertainty

Political uncertainty has done little to slow the markets, as evidenced by the immediate aftermath of Brexit and Donald Trump’s surprise victory. While major legislation hasn’t yet been passed in 2017, equities investors appear to be encouraged about how the administration’s pro-business agenda could impact them in the future.

5. An Equation is No Substitute for Monetary Policy

Some of the Fed’s critics suggest that monetary policy should be governed by a set of fixed rules, eliminating the need for a committee of economists to set interest rates. But an equation linking rate hikes to developments in unemployment and inflation would’ve likely been counterproductive during the recovery.

It’s easy to find points in the recent past when a strict rule-based monetary policy would’ve led to missteps. For example, when the headline unemployment rate underestimated the true level of slack in the labor market, a rule would’ve likely prescribed monetary tightening prematurely, restricting job growth when it was still needed. Additionally, when collapsing oil prices skewed inflation downward, a rule-based reaction might’ve missed the underlying strength in demand and left rates too low for too long, risking an overheated economy. In retrospect, the Fed has done admirably at promoting the recovery, and it’s hard to imagine an equation could’ve capably substituted for experienced judgment.

—Jim Glassman, Head Economist, Commercial Banking May 10, 2017

Comments