The new SECURE Act requires rethinking retirement planning

Posted By RichC on January 26, 2020

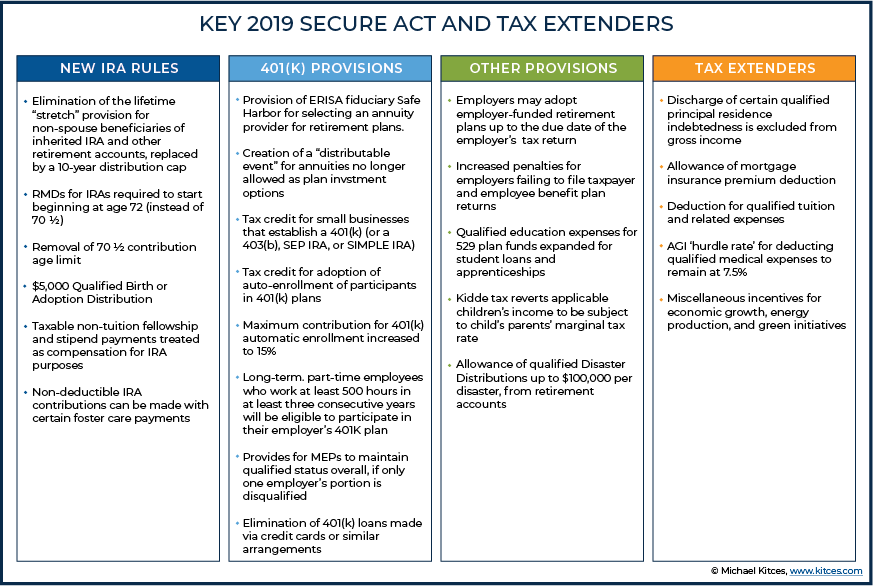

graphic credit – Enza Financial

There was an excellent podcast on Charles Schwab‘s WashingtonWise Investor (link) last week with Mike Townsend and Dan Stein that summarized the 2020 changes for those planning their retirement – hopefully everybody. Most of the new changes made by Congress last year in the SECURE Act are based on Americans living and working longer than in the past, hence one of the big changes has to do with RMDs (Required Minimum Distributions) from tax differed accounts used by Americans in saving for retirement (IRAs, 401Ks, etc). Oh, if you are wondering about the Washington DC acronym SECURE, it is: Setting Every Community Up for Retirement Enhancement.

living and working longer than in the past, hence one of the big changes has to do with RMDs (Required Minimum Distributions) from tax differed accounts used by Americans in saving for retirement (IRAs, 401Ks, etc). Oh, if you are wondering about the Washington DC acronym SECURE, it is: Setting Every Community Up for Retirement Enhancement.

The big change from my perspective is when we are required to take money out (and begin to pay taxes on) retirement savings that has been put aside pre-tax. Prior to the SECURE Act in 2020, that age as been 70½. Under the new law, you do not have to take distributions until the year you turn 72. The new rule gives more time for your retirement savings to grow before you need to begin drawing it down. That dollar amount come from an IRS published table based on life expectancy and the amount saved. Under the current rules, your first few RMDs are less than 4% of the account value, but they escalate as you get older, getting closer to 7% of the account value by age 85 and close to 9% by age 90.This is important because distributions from traditional retirement plans are taxed as ordinary income, so as the size of your distributions increase, your tax burden may as well.

Probably the other big change is how "inherited" IRAs are handled. Under current law, non-spouse designated beneficiaries can take distributions over their life expectancy, but for many retirement account owners who pass away in 2020 and beyond, beneficiaries will have ‘only’ 10 years to empty the account.

"On the one hand, without any other distribution requirements within those 10 years, designated beneficiaries will have some flexibility around the timing of those distributions; however, certain types of “see-through” trusts that have been drafted to serve as beneficiaries of retirement accounts may find that they’re no longer able to make annual distributions to the trust under the new rules (only to suddenly have both the IRA and trust forcibly liquidated at the end of the 10-year window)." – Michael Kitces link & graphic below

Comments