Primer: An retirement savings decision making cheat sheet

Posted By RichC on August 14, 2021

The older I get, the less investment risk I’m comfortable taking. Perhaps it is not the age thing, but having experienced stock market gyrations and what happens to our investments?

For those of us in small business or in the gig economy, and increasingly  for those who move from company to company, we are our own investment decision-makers. Even for those working at small companies, gone are the days of pensions and company managed investments. For much of America … this mean we are saddled with making decisions regarding saving and planning for your retirement. If you do it well, and stay healthy, then you’ll likely be more comfortable than those who rely on their employer or a government plan. If you do it poorly, your golden years are likely to be filled with regret.

for those who move from company to company, we are our own investment decision-makers. Even for those working at small companies, gone are the days of pensions and company managed investments. For much of America … this mean we are saddled with making decisions regarding saving and planning for your retirement. If you do it well, and stay healthy, then you’ll likely be more comfortable than those who rely on their employer or a government plan. If you do it poorly, your golden years are likely to be filled with regret.

So what are your options?

- A robo-advisor or pay an investment advisor or company a percentage of what you budget to make decisions for you. It is likely they’ll take at least 1% of your assets (likely more) every year whether they make you money or not (watch for the hidden cost too). It is a hard pill to swallow for those who may have independently made decisions their whole life (common for entrepreneurs).

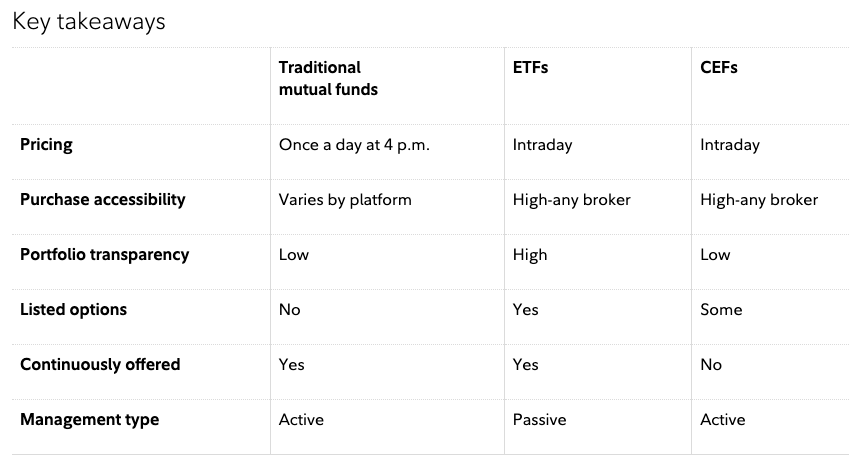

- Choose Mutual Funds which have long been the way individuals have saved and balanced the risk of owning individual stocks and bonds or having to make buy and sell decisions on the assets they hold. Mutual Funds have fees, but many are palatable and smaller percentages. They are easier to cut ties with (sell) if you don’t like their performance and fees or when your risk profile changes when you get older. Mutual funds are priced once each day at 4PM EST but are well design for those who might want to tweak only once or twice a year … if that?

- Open a brokerage account and trade Individual Stocks, Bonds (or CDs, life insurance plans and annuities, etc) – Those who are confident in their decision-making will be happy doing this, but statically they often fail to maintain stable portfolios or even keep up with the professional managers or Mutual Funds after paying fees. Buying single stocks can be is pretty risky and having only a few stocks is like closing your eyes and walking across a country road – probably safe but risky. Still, if consistently done right, you won’t be giving up the saved management fees .. and they can compound year after year and be retained in your portfolio.

- Finally there are ETFs and CEFs. This last segment is becoming increasingly popular since the combination and variety ETFs and CEFs along with online screening tools can help reduce risk and cost. They offer a wide variety of investment options (too many choices) and reduce risk by holding a bucket of stock, etc in one ticker symbol (diversity within similar assets). They can be strictly “index-tracking” related shares or structured to change based on your age. The assets are passively managed (low fees) in the case of ETFs, or actively managed by professionals with those associated risks, but can reward with better returns and higher dividends for their higher fees in the case of CEFs. The advantage for those who want to trade more often, in these days of low and no commissions, is that they can be bought and sold throughout the trading day.

The learning center at Fidelity had a great chart and write-up that might be helpful … and helpful enough to archive below.

Closed-end funds vs. mutual funds and ETFs

A common misunderstanding is that a closed-end fund (CEF) is a traditional mutual fund or an exchange-traded fund (ETF). A closed-end fund is not a traditional mutual fund that is closed to new investors. And even though CEF shares trade on an exchange, they are not exchange-traded funds (ETFs).

CEFs share some traits with traditional open-end mutual funds

- Both have an underlying portfolio of investments with a net asset value

- Both are run by a professional management team

- Both have expense ratios and, typically, fee schedules

- Both may offer distributions of income and capital gains to investors

However, traditional mutual funds issue and redeem shares daily, at the end of business, at the fund’s net asset value. CEFs do not issue or redeem shares daily. Instead, CEF shares trade on an exchange intraday, like stocks. The share price for a CEF is set by the market. The share price only rarely, and by sheer coincidence, equals the CEF’s net asset value. Also unlike traditional mutual funds, CEFs may issue debt and/or preferred shares to leverage their net assets. That leverage can increase distributions (income) but also increases volatility of the net asset value.

CEFs share some traits with ETFs

- Both have an underlying portfolio of investments with a net asset value

- Both trade during the day on exchanges

- CEF and ETF shares can be treated very much like a stock, in that you can set limit orders, short the shares, and buy on margin

- The portfolios may be leveraged

- Both have expense ratios and, typically, fee schedules

- Both may offer distributions of income and capital gains to investors

ETFs have a redemption/creation feature, which typically ensures the share price doesn’t stray significantly from the net asset value. As a result, an ETF’s capital structure is not closed. CEFs do not have such a feature. CEFs are actively managed, whereas most ETFs are designed to track an index’s performance. CEFs achieve leverage through issuance of debt and preferred shares, as well as through financial engineering. ETFs are precluded from issuing debt or preferred shares. ETFs are structured to shield investors from capital gains better than CEFs or open-end funds are.

Comments