Local banking issues, blockchain technology and the interesting book: Crypto Asset Investing in the Age of Autonomy

Posted By RichC on August 15, 2021

For decades now I’ve had a fairly positive relationship with both business (CPP) and personal banking … and particularly with local banks. I grumbled the 1990s when multiple bank mergers forced out the manager I worked with in NE Ohio. He knew me by name and often pulled me aside to see if there was anything my business needed. That was helpful for a small business owner and it was appreciated when starting a business. Unfortunately the changes brought “less personal” banking to both the small business and personal side … BUT we adapted and even learned to appreciate the efficiency improvements online banking brought us.

me aside to see if there was anything my business needed. That was helpful for a small business owner and it was appreciated when starting a business. Unfortunately the changes brought “less personal” banking to both the small business and personal side … BUT we adapted and even learned to appreciate the efficiency improvements online banking brought us.

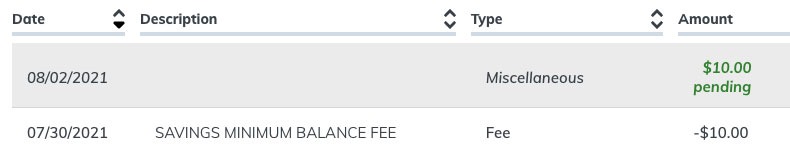

Lately though (the last decade perhaps), it seems banks are becoming desperate in squeezing existing customers and are looking for ways to make a buck here and there; it has been irritating and even a lot less personal (if that is possible). Recently a sneaky $10 fee for not “maintaining a $2500 DAILY balance” on a linked savings account surprised me. Even worse was that the Huntington Bank local branch couldn’t solve my minimal gripe, didn’t have current interest rates and didn’t know the balance requirements for their savings accounts. I ended up wasting a half hour on hold in  order to talk with a customer service representative for him to tell me the minimum daily balance was $2500 … yet he still could not tell me what the interest rate was nor could he close out my offending account, although I did get the $10 charge reversed. If we are not receiving friendly personal service (or interest on account balances), why should we bank locally if all they are doing is using gimmicks to entice new and existing customers to open new and additional accounts then … drive them off by charging monthly fees? (although it is not quite the “open an account, get a toaster” from my mom and dad’s generation)

order to talk with a customer service representative for him to tell me the minimum daily balance was $2500 … yet he still could not tell me what the interest rate was nor could he close out my offending account, although I did get the $10 charge reversed. If we are not receiving friendly personal service (or interest on account balances), why should we bank locally if all they are doing is using gimmicks to entice new and existing customers to open new and additional accounts then … drive them off by charging monthly fees? (although it is not quite the “open an account, get a toaster” from my mom and dad’s generation)

The whole fiasco has me wondering if banks, and in particular local banks, are doomed once cryptocurrency digital wallets and connected smart device like watches and phones using blockchain technology go mainstream?

As for the book, my buddy Jeff loaned me an interesting blockchain – cryptocurrency book to read by Jake Ryan called “Crypto Asset Investing in the Age of Autonomy” and he likely is waiting on my thoughts and opinion (we tend to discuss these kinds of things).  Of course I’ve been intrigued and frightened in watching so many in our society (especially the millennials) leaping onboard without understanding where they are sending their money and what they are buying/trading/investing in … pick your description. I’ve been a fractional shares holder for a couple of years now and am reluctant to call buying Bitcoin, Ethereum, etc “investing” since it current resembles an unregulated artificial asset that resembles a pyramid scheme … or probably more appropriately a privately traded “currently” non-functional currency without something tangible behind it like a precious metal, a commodity, share of a company or even a fiat currency issued by a government. Crypto advocates of all flavors are quick to point out that most other assets we hold that do not have intrinsic value either and are priced in a similar supply-demand fashion … Hunter Biden’s artwork comes to mind (ok, that was a joke … or should I say IS a joke).

Of course I’ve been intrigued and frightened in watching so many in our society (especially the millennials) leaping onboard without understanding where they are sending their money and what they are buying/trading/investing in … pick your description. I’ve been a fractional shares holder for a couple of years now and am reluctant to call buying Bitcoin, Ethereum, etc “investing” since it current resembles an unregulated artificial asset that resembles a pyramid scheme … or probably more appropriately a privately traded “currently” non-functional currency without something tangible behind it like a precious metal, a commodity, share of a company or even a fiat currency issued by a government. Crypto advocates of all flavors are quick to point out that most other assets we hold that do not have intrinsic value either and are priced in a similar supply-demand fashion … Hunter Biden’s artwork comes to mind (ok, that was a joke … or should I say IS a joke).

As I started reading the “Author’s Note” section, I was immediately intrigued since the author is a much bigger thinker than the narrow mind of someone who just wants to know which cryptocurrencies to buy and which avoid (thinking like a stockpicker). The point Mr. Ryan quickly makes is how much like the “Industrial Age” and “Information Age” … he believe we are in the “Age of Autonomy” where blockchain technology is going to be the way people gain back control of their personal information. If you don’t see it currently, much of big tech for the most part is in the business of collecting your personal information. They then either sell it or market using it … or both. It is one thing when AI scans your social networks and Gmail in order to help sell you what you want (or might want) … it is another when it builds a profile that has everything from your health information, politics, purchase history, who you communicate with and every place you have been for as far back as you’ve been freely giving them your GPS locations. (Check out the Netflix movie: The Social Network – preview)

Competition, the drive for efficiency, and continuous improvement ultimately push businesses toward automation and later towards autonomy. If a business can operate without human intervention, it will minimize its operational cost.

If Uber can remove the expense of a driver with an autonomous vehicle, it will provide its service cheaper than a competitor who can’t. If an artificially intelligent trading company can search, find, and take advantage of some arbitrage opportunity, then it can profit where its competitors cannot. A business that can analyze and execute in real-time without needing to wait for a human to act, is a business that will be able to take advantage of brief inefficiencies from other markets or businesses.

This trend following a thesis that is based on 100 years of proven economic theory. Short-wave economic cycles, those 5- to 10-year cycles, are driven by credit but the long-wave economic cycles, those 50- to 60-year cycles, are driven by technological revolution. We’ve had 5 cycles over the past 200 years with the last wave, the Age of Information & Telecommunications.

We’ve seen evidence that a new cycle has begun. Technological revolutions come by way of a cluster of new innovations. About a decade ago, you started to see AI, robotics and IoT (sensors) delivering on automation. That’s been powerful, but not transformational. It does not force businesses to fundamentally change how they do business. The last piece of the puzzle was cryptocurrency because it allows us to process and transfer economic value without human intervention. Soon, there will be a global race to build autonomous operations. Businesses and organizations without autonomous operations simply will not be able to compete with those that do because … autonomy is the ultimate competitive advantage.

Crypto is the mechanism that will accrue value from being the infrastructure for the next digital financial revolution. Crypto Asset Investing lays out a case that we’ve begun a new technological revolution similar to the Internet Age of the 1990’s. Artificial intelligence, the Internet of Things, robotics and cryptocurrency are converging to deliver on a new age, what I call the Age of Autonomy. Understanding the transformation that’s taken place before anyone else can yield enormous investment opportunity. In this book, you’ll learn how and why to invest in crypto assets.

Comments