The Silent Theft: Dollar Devaluation and Persistent Inflation

Posted By RichC on July 16, 2026

For generations, Americans have been told that saving, investing wisely and planning for retirement embody the virtues of self-reliance and prudence. Yet today, many on fixed or semi-fixed incomes — pensions, annuities and even Social Security — are watching those plans quietly unravel. The culprit? The steady devaluation of the U.S. dollar driven by chronic inflation.

As of mid-2026, headline inflation has climbed back toward 4.2%. While lower than the peaks of recent years, this compounds a deeper, decades-long erosion. The purchasing power of the dollar has plummeted: what $1 bought in the early 1980s (around the CPI base) now requires over $3. A retiree relying on $50,000 annually in today’s dollars could see that buy only about half as much in 25-30 years at average 3% inflation — devastating for those without growth assets.

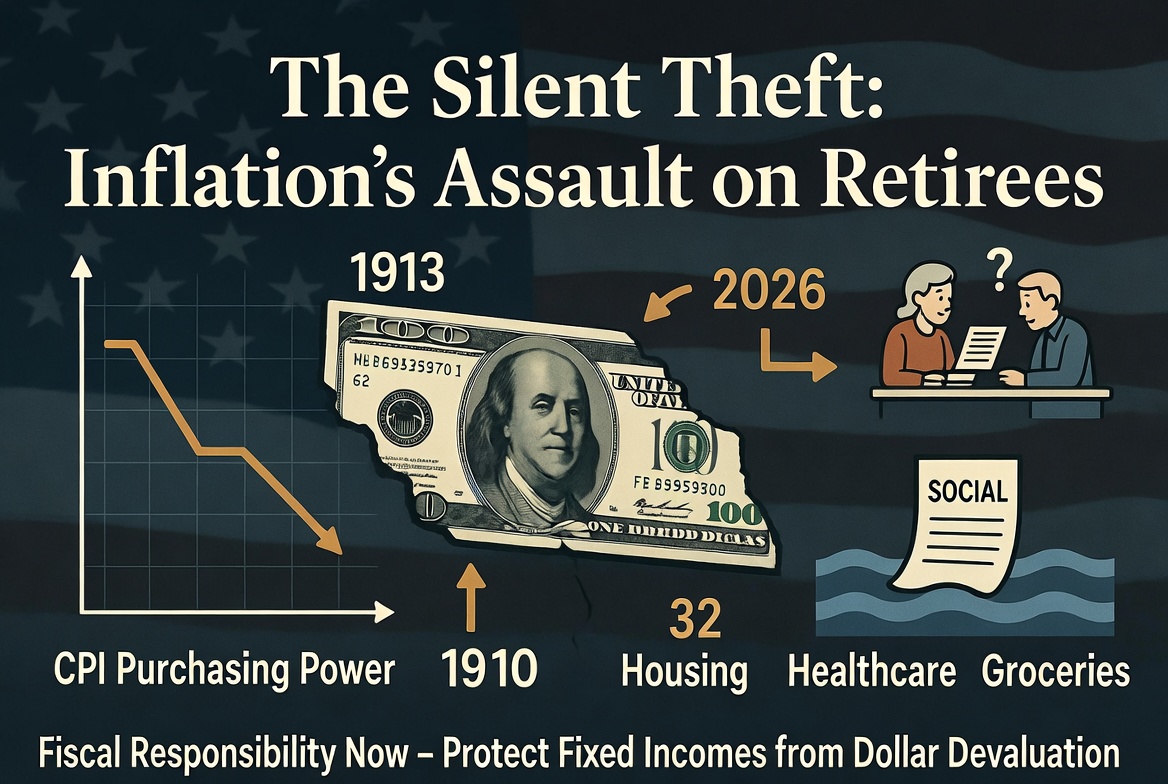

Fixed incomes and annuities look solid on paper —

until inflation erodes their real value over decades.

Retirees feel this acutely. Social Security offers cost-of-living adjustments (COLAs), but these often lag real expenses like healthcare and housing, which rise faster for seniors. Annuities and traditional pensions, popular for their “guaranteed” payments, deliver nominal dollars that buy less each year. A weaker dollar also inflates import costs and can fuel broader price pressures, pinching budgets already stretched thin.

Those who delayed claiming benefits or coordinated spousal strategies to maximize lifetime income (smart moves) still face the reality that inflation doesn’t pause for prudent planning. Semi-fixed incomes from part-time work or dividends offer some buffer, but without hedges, the math turns against savers.

This isn’t mere bad luck — it’s policy failure. Decades of runaway federal spending, trillion-dollar deficits and a national debt nearing $40 trillion have pressured the Federal Reserve to monetize obligations through expansive monetary policy. When government prints or borrows without restraint, it dilutes the currency’s value. Conservatives have long warned that big-government programs, endless entitlements and emergency spending create moral hazard and economic distortion. Inflation acts as a hidden tax, disproportionately harming those on fixed incomes who can’t easily adjust — precisely the responsible citizens who played by the rules.

Loose money favors debtors (including Washington) at the expense of creditors and savers. It distorts markets, encourages malinvestment and undermines the stable dollar essential to free enterprise. Younger generations may adapt through higher earnings or asset appreciation, but retirees cannot.

No one can fully escape macroeconomic forces, but individuals can mitigate risks:

- Diversify beyond fixed income: Favor assets with inflation-hedging potential — productive businesses (stocks), real estate or commodities — while maintaining balance due to volatility.

- Review annuities and bonds: Consider inflation-protected options like TIPS where suitable, or laddered strategies.

- Maximize indexed benefits: Optimize Social Security and pensions; track personal COLAs against actual spending.

- Control what you can: Reduce debt, build flexible budgets and support fiscal policies that prioritize balanced budgets, spending restraint and monetary discipline.

Fiscal conservatives should advocate for entitlement reform, debt reduction and a Fed focused on price stability rather than engineering outcomes. Sound money preserves liberty; inflation erodes it.

The devaluation of the dollar isn’t abstract economics — it’s a long-term threat to the American Dream of dignified retirement. Those who saved diligently deserve better than a government-induced slow bleed. By highlighting these realities and pushing for accountability, we can encourage policies that value savers over spenders. For retirees and near-retirees: plan defensively, live prudently and demand better from our leaders. Your fixed income depends on it

Comments