The confusing world of Credit Scores

Posted By RichC on November 29, 2009

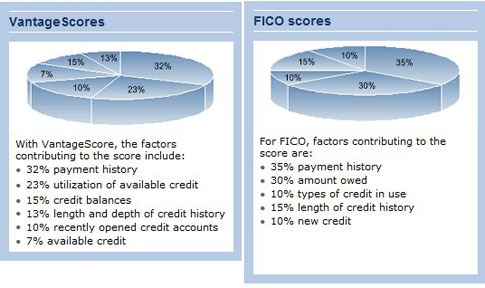

I’ve blogged couple times on identity theft and credit reports and I thought was relatively up-to-date on on how credit reporting and ‘credit scoring’ works … but I was wrong. I didn’t realize that the three major credit collecting and reporting companies all have their own “credit scoring system” on top of the relatively popular Fair Isaac Corporation’s “FICO” score (300-850) that most of us are familiar with. The fact that they do have their own ‘scoring’ systems which have different scales make it all the more confusing. (credit tracking) If that’s not enough, the three companies have also collaborated to create a VantageScore (501-990) which has a different scale as well.

This was particular interesting since when viewing a yearly annual credit report in order to monitor for identity theft. One of the optional choices available when ordering a ‘free’ credit report (for an added fee) is your credit score. These are the numbers most companies use in order to evaluate instant credit. Unfortunately unless you are requesting the FICO score (estimate your FICO score), you could be getting individual TransUnion, Experian or Equifax number … or the newly adopted VantageScore. Although all give a picture of credit health, the number doesn’t necessarily mean all that much if you’re not familiar with the scale.

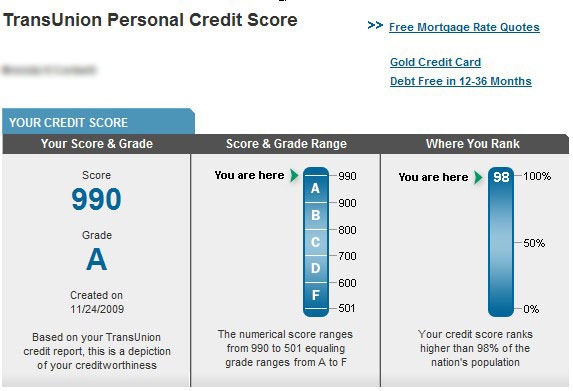

The FICO’s scale is a 300 to 850, while the VantageScore goes from 501 to 990 and is graded A to F:

A: 901–990 | B: 801–900 | C: 701–800 | D: 601–700 | F: 501–600

—

More Information:

Comments