What is and are the criteria for a good FICO credit score?

Posted By RichC on December 2, 2014

In talking with a long time customer today about shopping and using credit cards, the subject of FICO scores came up  since they are printed each month on Discover Card statements (nice touch Discover). He ask me what a good score was and I “sort of” knew that over 700 was good and thought 760 was excellent, but could give him a definitive answer even though I’ve blogged on this topic a couple times before. Instead of guessing I looked up the information and found an excellent graphic (below) and helpful pie chart (above) explaining what is used to calculate a credit score (adding a WSJ PDF titled: “What is a FICO Score?“).

since they are printed each month on Discover Card statements (nice touch Discover). He ask me what a good score was and I “sort of” knew that over 700 was good and thought 760 was excellent, but could give him a definitive answer even though I’ve blogged on this topic a couple times before. Instead of guessing I looked up the information and found an excellent graphic (below) and helpful pie chart (above) explaining what is used to calculate a credit score (adding a WSJ PDF titled: “What is a FICO Score?“).

After a little searching online, I noticed Credit.org posted a great charge and set of numbers earlier this year. Check out their blog post or click the graphic for a larger version.

According to Credit.org …

It’s difficult to get exact answers to this important question. Every expert, credit bureau, and loan officer has a different opinion as to where the threshold between good and poor credit lies. In addition, “good” can be a relative term. Do we mean “good” as in excellent, or “good” as in “good enough”?You can start by comparing your score to national averages. According to FICO, the following proportions of consumers have scores in the following ranges:

- Up to 499: 2%

- 500-549: 5%

- 550-599: 8%

- 600-649: 12%

- 650-699: 15%

- 700-749: 18%

- 750-799: 27%

- 800-850: 13%

You can see that over 50% of the population has a credit score over 700, with 42% scoring below that level.

Lower credit scores aren’t always the result of late payments, bankruptcy, or other negative notations on a consumer’s credit file. Sometimes, a consumer who doesn’t have enough information on his/her file will have a low score. This can happen even if you had established credit in the past; if your credit report shows no activity for a long stretch of time, items may ‘fall off’ your report. (This is because your credit score must have an update provided by your creditor within the past six months; if you creditor stops updating an old account you don’t use, it will disappear from your credit report and leave FICO with too little information to calculate a score.)

Similarly, consumers new to credit will have no established credit for FICO to use when calculating a risk score. If there is just a little bit of information, you may get a score, but it may be low. This low score wouldn’t be because you made any mistakes, but because you are considered a risky borrower because the credit bureaus don’t know enough about you.

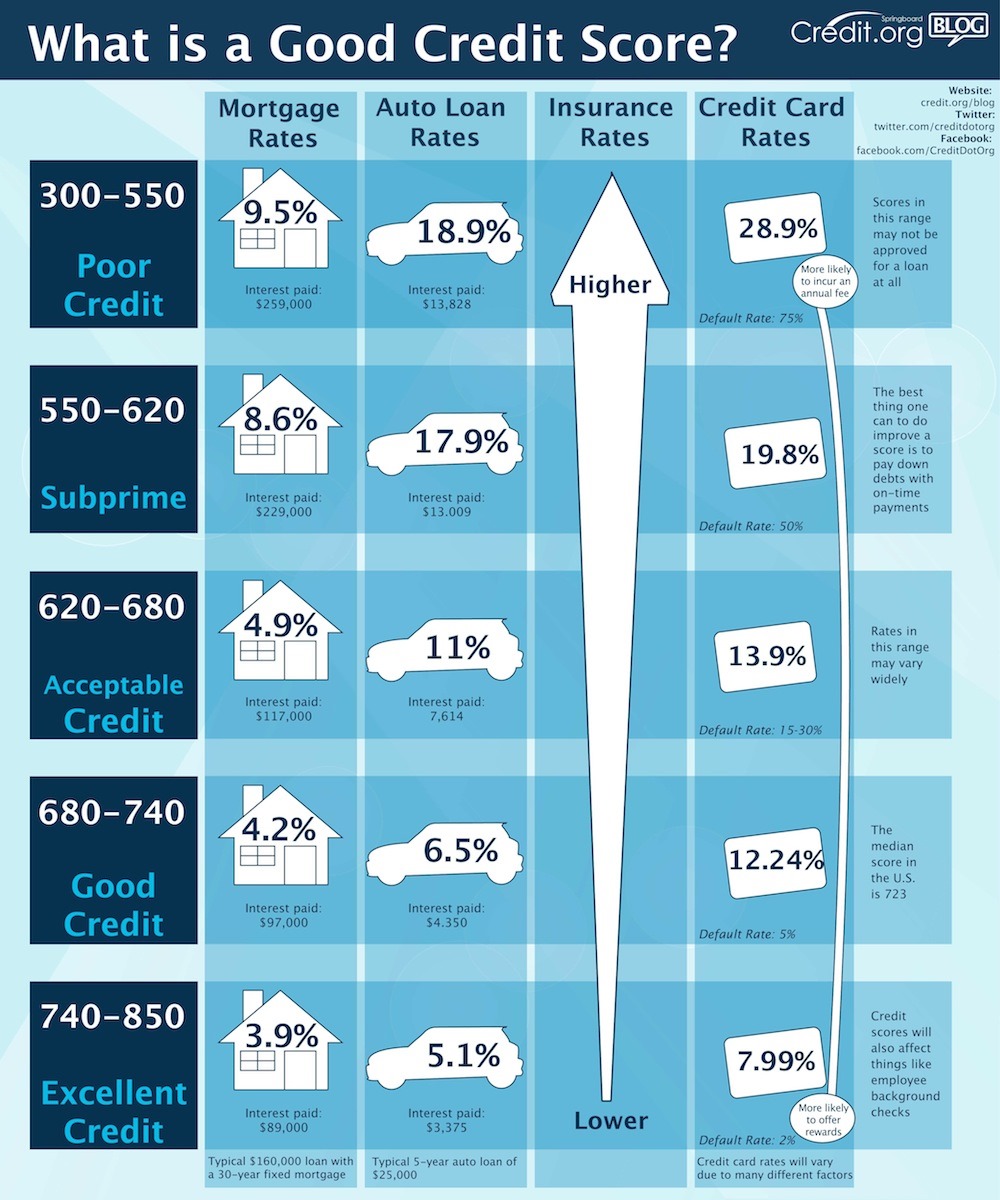

Let’s explore the numbers. Credit scores range from 300 to 850, with higher scores being better. Here’s a rough guide to what various score ranges mean:300-550: Poor credit. It is generally accepted that credit scores below 550 are going to result in a rejection of credit every time. If your score has fallen into this range, you need to work to improve your score. Often a bankruptcy filing will bring a score down to this level; over time, the score will improve if you make your payments on time, every time. Statistically, borrowers with scores this low are delinquent approximately 75% of the time.

550-620: Subprime. It’s possible to get credit in this range, but not guaranteed. If you do get a loan, it will be at very disadvantageous terms: you will pay much higher interest rates and penalty fees. In this range it is worthwhile to address any specific credit problems you have and try to boost your score before applying for credit. In this range, borrowers typically become delinquent 50% of the time.

620-680: Acceptable. Scores in the mid 600’s mean you will most likely be given credit when you apply for it. You still won’t get the best interest rates, but borrowers with scores over 620 are considered less risky and are therefore likely to be approved. In this range, borrowers can expect to qualify for a prime rate. Traditionally, “Prime” loans could be easily sold to Fannie Mae or Freddie Mac. Delinquency rates in this range are between 15 and 30%.

680-740: Good credit. Scores around 700 are considered the threshold to “good” credit. Borrowers in this range will almost always be approved for a loan, and be offered very good interest rates. At this credit score, lenders are comfortable with the borrower, and the decision to extend credit is much easier. According to FICO, the median credit score in the U.S. is in this range, at 723. Borrowers in this range are only delinquent 5% of the time.

740-850: Excellent credit. Anything in the mid 700’s and higher is considered excellent credit, and will be greeted by easy credit approvals and the very best interest rates. In this high-end of credit scoring, extra points don’t improve your loan terms much. Most lenders count a credit score of 760 as just as good as a score over 800. Some people take this to mean that it’s not worth the effort to continue to improve your score after you get into this range, but as always, the higher your score, the better. Even if an extra 50 points in this range doesn’t help you get a better interest rate on your next loan, they can serve as a buffer if you have a negative item show up on your report (maxing out a credit card can penalize you 30-50 points. If your score is near 800, the resulting damage won’t push you down into a lower tier). The delinquency rate in this range is approximately 2%.

Of course, different lenders have different standards, and your experience may vary. You may have a high credit score, but a negative public record on your credit file may hurt your chances of getting a loan. And remember, while credit scores don’t take your income into account, lenders will, and if they feel you simply can’t afford the loan you’re applying for, they won’t approve you no matter how good your score.

So you can see that getting to a score in the mid 600’s might enable you to qualify for credit, but a score of 680 or above is the threshold for “good” credit. And if you can get your score up to the mid 700’s, your credit will be considered excellent, and you will have few worries when it comes to qualifying for credit at favorable rates.

Comments