Debt, Bankruptcy and Loan Forgiveness — a personal rant

Posted By RichC on December 15, 2016

Forgiving debt and bankruptcy options aren’t new, but those of us who strive to “play by the rules” often feel like suckers when it comes to bureaucrats playing fast and free with tax dollars … or with OPM. While it is understandable that our society wants to be compassionate and lend a helping hand to our fellow citizens who are down on their luck or experiencing an unforeseen change in circumstances …  accepting an ongoing system which releases the obligation of debt and loans just encourages more of the same.

accepting an ongoing system which releases the obligation of debt and loans just encourages more of the same.

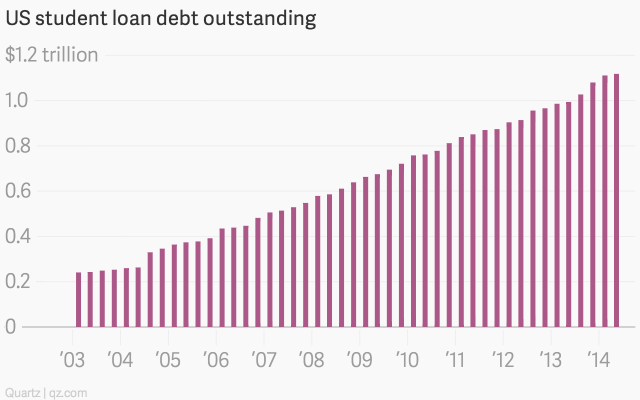

As with the subprime mortgage crisis in the mid-2000s, a recent article in the Wall Street Journal addressed the looming Student Loan problem and debt young people voluntarily take on in order to attend college. Too many are enticed and even encouraged to accept the “easy loans” without weighing the long term consequences. Most students aren’t financially astute enough to make sense of the BIG $$$ numbers when they accept loans as a way of funding sky-high tuitions, country club accommodations and even overseas abroad travel. Postponing the payback pain seems to be “acceptable” when borrowing for an education, a credit card binge or any of the other easy to get loans. The hole is too easy to start digging and way too easy to dig deep. I’ve heard in debt students say their only other option is flipping burgers, living at home and scrimping to save for college one semester at a time … who wants to do that?

Unfortunately the answer many “vote hungry” politicians (and a particular political party) are answering debtors pleas with a loan forgiveness program; but wouldn’t a robust economy and improving wages through a robust economy be a better solution? Debt forgiveness is their way of fixing what is being described as an “unprecedented surge in student loan debt” … it only encourages others to practice irresponsible behavior … “hey, I want a free education too!” The solution currently is back by the Obama administration, “will likely provide the biggest benefits to newer graduates who immediately enter into the program. Older borrowers who have been paying down their debts for years can’t retroactively apply those payments when entering into an income-driven plan, due to a quirk in the law” (those grads aren’t happy). Hearing this, it is difficult to give sound advice to students and parents contemplating the “smart way” to fund a college education. (“smart” being the word President-Elect Trump used to explain bankruptcies and using the structure of a complex tax code to pay few if any federal taxes – link ).

From the WSJ article: Student-Loan Forgiveness Irks Borrowers

The plans also provide the biggest subsidies to borrowers with the largest balances. Government data show those tend to be graduate-degree holders and high earners. Borrowers with smaller balances will often pay more than they would have under a standard 10-year plan due to interest accrual.

And in some cases, two workers doing the same job get different subsidies. For example, a nurse working for a nonprofit hospital would get potentially tens of thousands of dollars more in forgiveness than one working for a for-profit employer, because of a provision Congress created to promote work in the public sector.

That provision—known as public service loan forgiveness—forgives balances after 10 years, tax-free. Private-sector workers have balances expunged in 20 or 25 years and are taxed on the forgiven amount.

The debt-relief programs “favor groups in arbitrary ways that aren’t really reflective of service or most people’s sense of fairness,” said Alexander Holt of the left-leaning think tank New America.

For many who have diligently worked and saved to help pay for college … or opted to go to more affordable schools, or perhaps pursued a trade-based profession, they see this new student loan forgiveness program as a slap in the face. A dad paying for his son to study at OSU commented, “why should long term professional students pursuing a PhD be traveling abroad on student loans and expect them to be forgiven?” Yup, when you hear this, why would responsible parents bother saving to help there children go to college or expect students to work part-time to help pay their expenses — instead just borrow more, enjoy school, take that semester abroad and apply for student loan forgiveness when you’re finished.

Where’s the wisdom in paying for things responsibly?

Comments