A Linux Server update and screenshots from a CRFB webinar

Posted By RichC on June 25, 2025

While updating a few more Linux server items elsewhere today, I learned a little bit more that might help out my older “droplet” that refuses to function the way I want due to so much old software. Yes … overdue for an overhaul, but the older I get, the more comfortable and set in my ways I become.

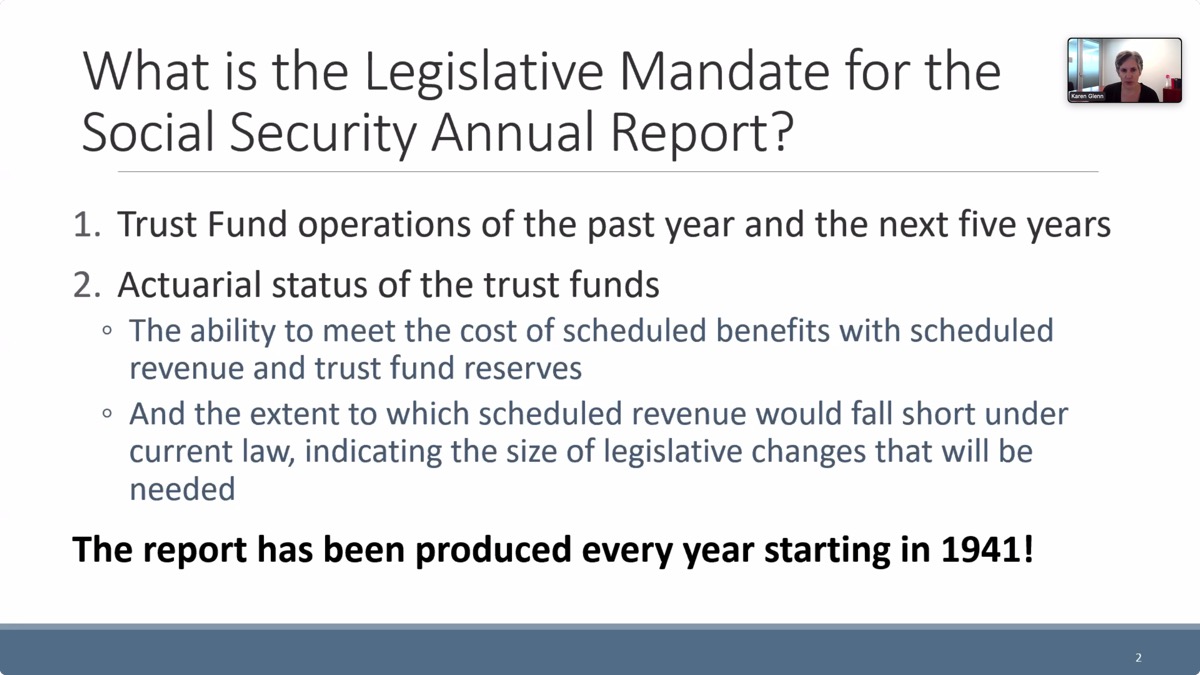

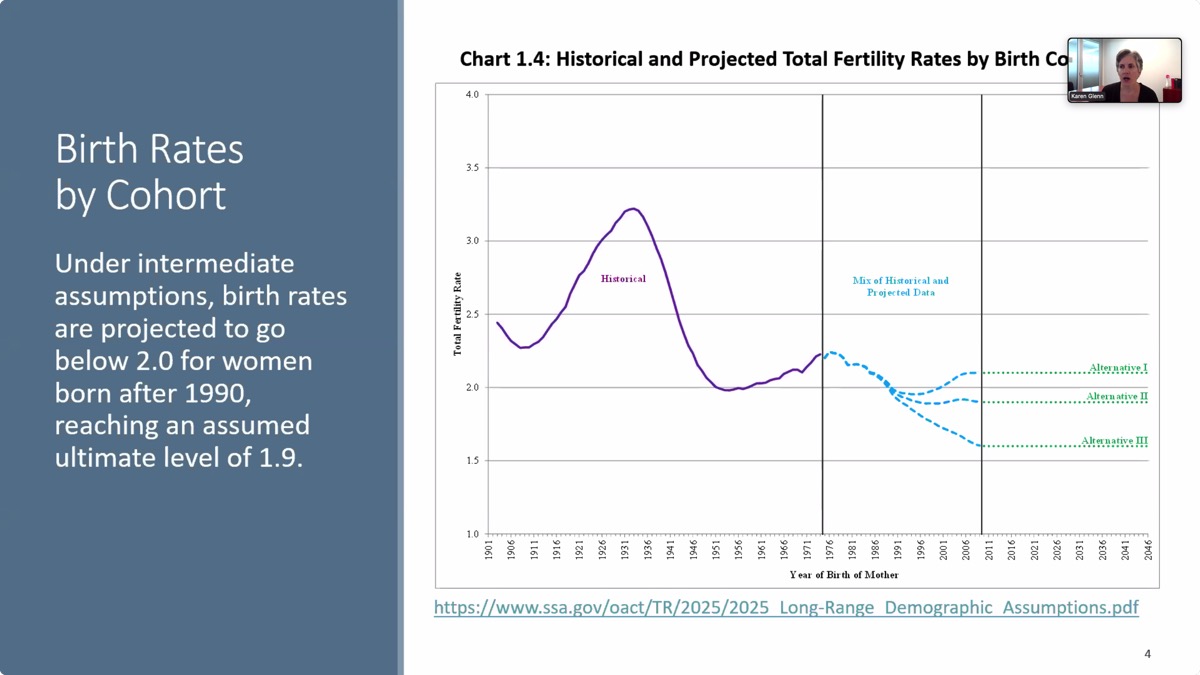

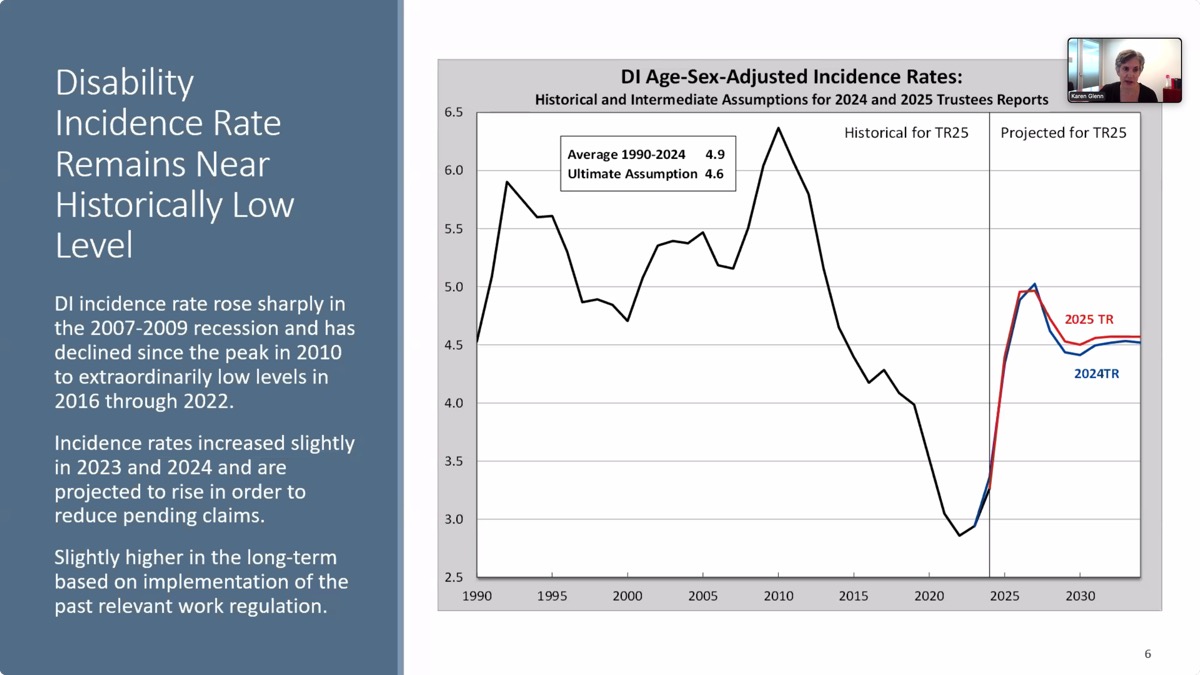

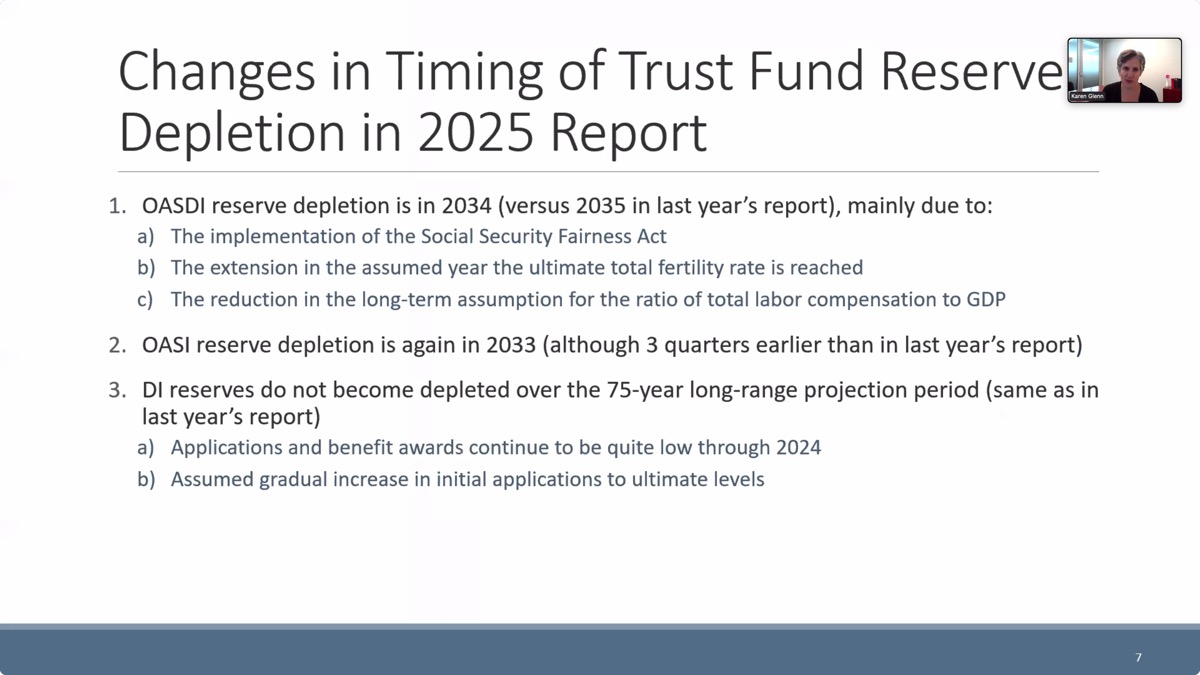

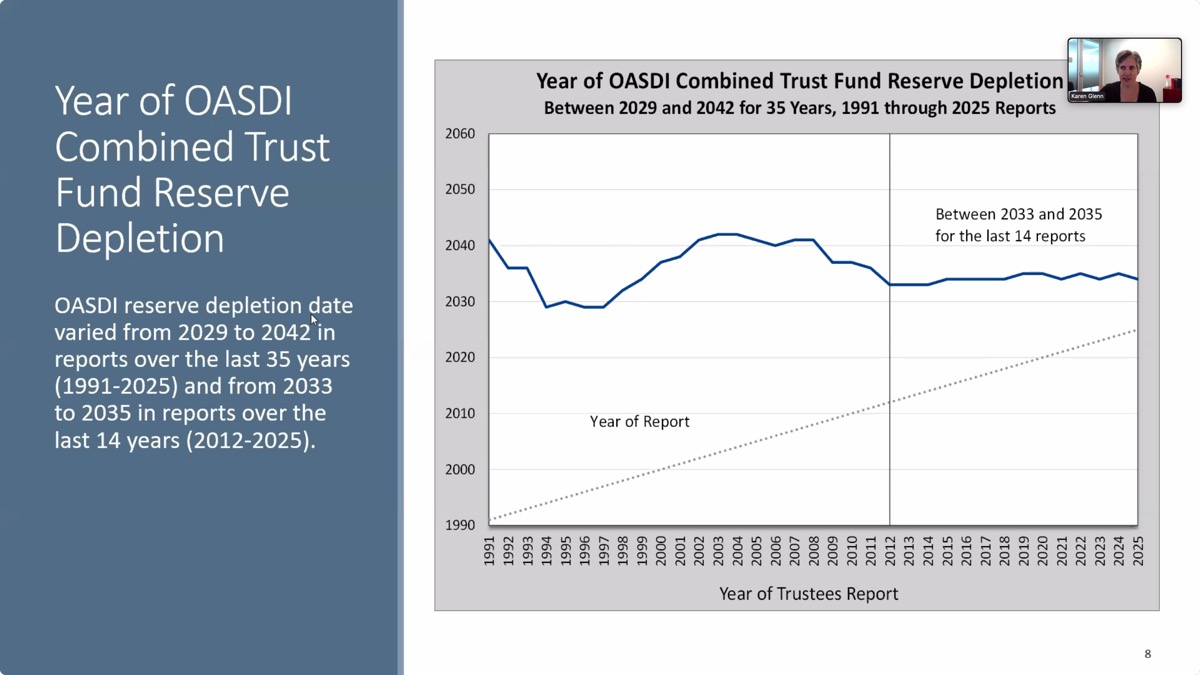

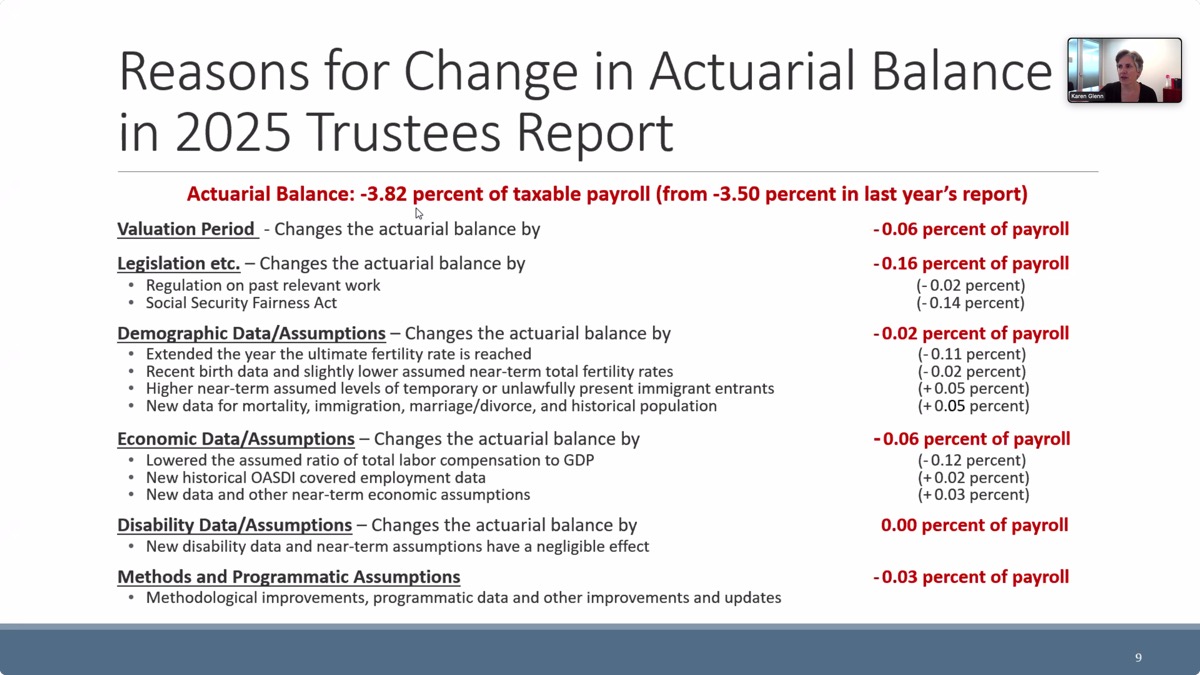

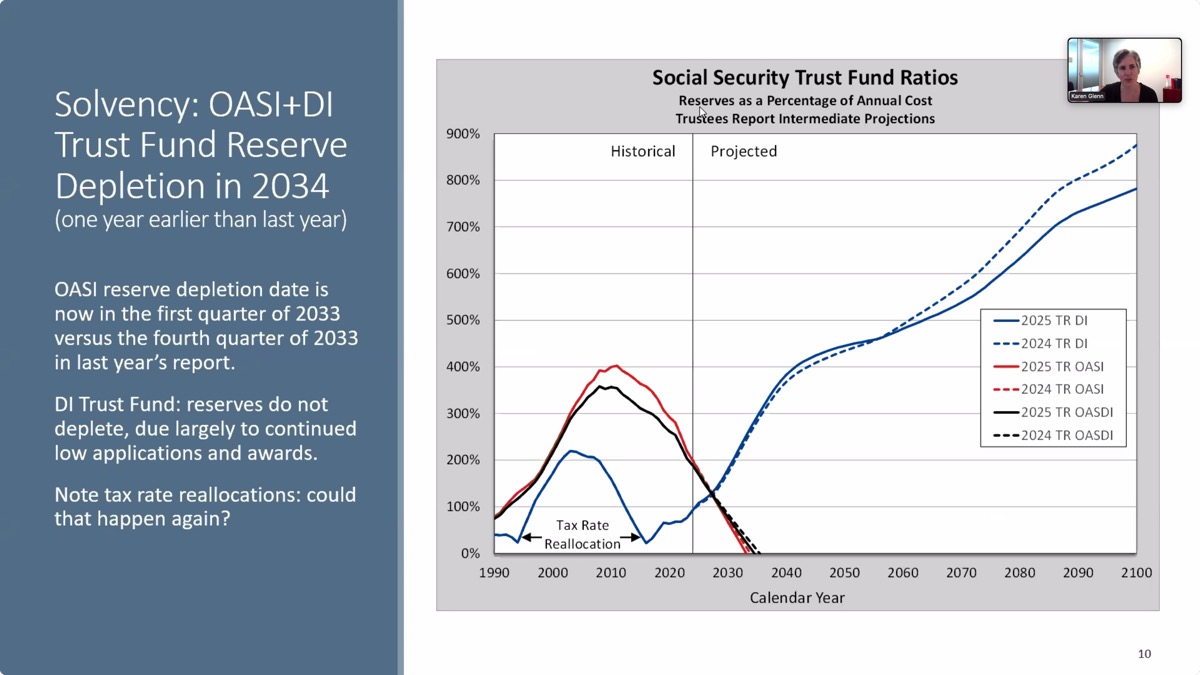

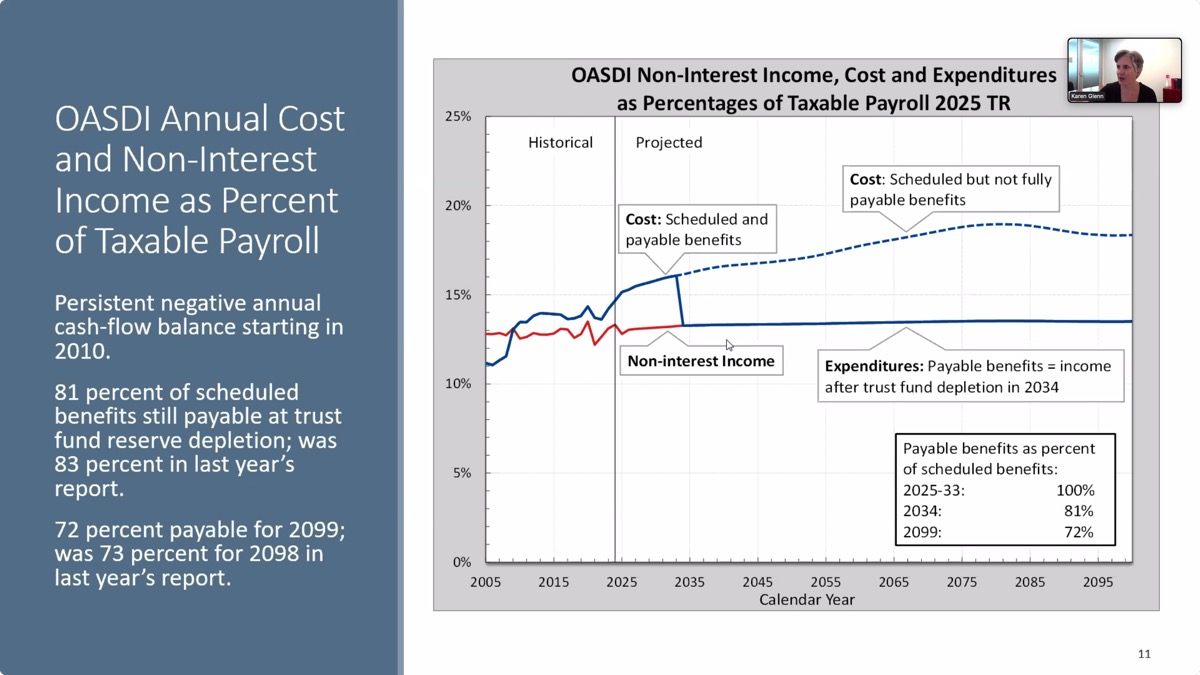

This late day post is merely a test and an excuse to post a bunch of screen grabs from a Social Security and Medicare webinar I attended yesterday — nice job by CRFB.org.

The Committee for a Responsible Federal Budget is a nonpartisan, non-profit organization committed to educating the public on issues with significant fiscal policy impact.

Our bipartisan leadership comprises some of the nation’s leading budget experts, including many past heads of the House and Senate Budget Committees, the Congressional Budget Office, the Office of Management and Budget, and the Government Accountability Office.

As an independent source of objective policy analysis, we regularly engage policymakers of both parties and help them develop and analyze proposals to improve the country’s fiscal and economic condition. These efforts have reinforced the Committee’s role as an authoritative voice for fiscal responsibility and an educational resource for policymakers and the general public. We are also a trusted budget watchdog that assists journalists across the country in understanding fiscal developments in Washington.