By DANA WECHSLER LINDEN Aug. 29, 2016 9:00 a.m. ET

New research raises the intriguing possibility that eating more fruit during pregnancy could boost the intelligence of a normal, healthy baby.

Researchers found that each additional daily serving of fruit that pregnant women consumed corresponded with an increase in cognitive scores for their children one year after birth. The study, at the University of Alberta, analyzed data from 688 children in the Canadian Healthy Infant Longitudinal Development, or Child, study.

The findings, published in the journal EBioMedicine in April, are preliminary and best seen as a suggestion for future studies on mammals and in randomized human trials, experts say. Still, the study is striking. Only one other food—fish—has been linked to enhanced cognitive development in normal, healthy offspring, experts say.

There may still be a few wanting a return to traditional values and morals … or at least I still believe Americans know there is right and wrong deep in their hearts. Our country is heading down a dark path, one that we seen throughout history, at least by most who have studied the Old Testament or pondered the Biblical prophesy for our future. Food for thought when given the opportunity to vote on issues or for a candidate who “may” strive to support Biblical values.

It is not all that unusual to have storms roll though on hot summer afternoon/evenings, but the dark skies with wind and lightning keeps me attentive to the weather after recent damage in Indiana as well as Ohio(or a Lightening Bolt Killing 323 Reindeer in Norway!) We had a hot weekend with temperatures in the 90s (continuing this week) and I found myself in and out of the pool while "pretending" to accomplish project in the garage (temps in my shop garage on my Dad’s old Packard thermometer above).

On my drive home this week, our 2010 BMW X5 35d modified diesel rolled the odometerpassed 150K (I know, they don’t roll like my old Mercedes anymore). Economy is not quite up to the 30 mpg highway that I have been hoping for, but I’m not complaining about 28 mpg "with an impressive power" for a full size 2-1/2 Ton SUV … made in Spartanburg, SC by the way. Once all the upgrades and tuning mods this past year were dialed in (358hp / 542 ft/lb TQ), the drivability and code clearing routine have been painless.I’m finally happy with this vehicle … and the seal of approval was hearing my wife say, "can I have MY car back?"

Using the equity in a home isn’t anything new, but I’m old enough to remember when "we" first started to tap into home equity with Home Improvement Loans. "Back in the day" IRS deductions for interest on consumer credit (car loans, revolving credit, signature loans) were being phased out for all but home mortgages. Creative homeowners and bankers soon found ways around the loss of interest tax deductions and found that "improving ones home" added equity and could therefore be consider deductible on taxes. As the practice grew, as did the terms and the "collection of receipts for everything spent on a home" … even if the money from newly accessed home equity from either a Home Equity Loan or HELOC was fungible.

Welcome to a loosening of tax policies and the renamed loan … now a Home Equity Line of Credit. Fewer restrictions and audits by the IRS gave homeowners readily accessible money at far more attractive rates than car loans, credit cards and signature loans. This became the boomers "bank" as they could continue to save for college and retirement while accessing cheap money utilizing they home as collateral. In the 1990s and 2000s many used the equity in their homes for "big purchases" … cars, college for their kids, wedding, etc. In the early years, few used HELOCs for general shopping or even vacations … and kept those items on month to month "plastic" credit cards. The banks felt secure in believing the lien on an "appreciating" home would protect them and this new financing was a great way to make money and keep customers happy … that was until it didn’t. (An aside: HELOC abuse is often cited as one cause of the subprime mortgage crisis.)

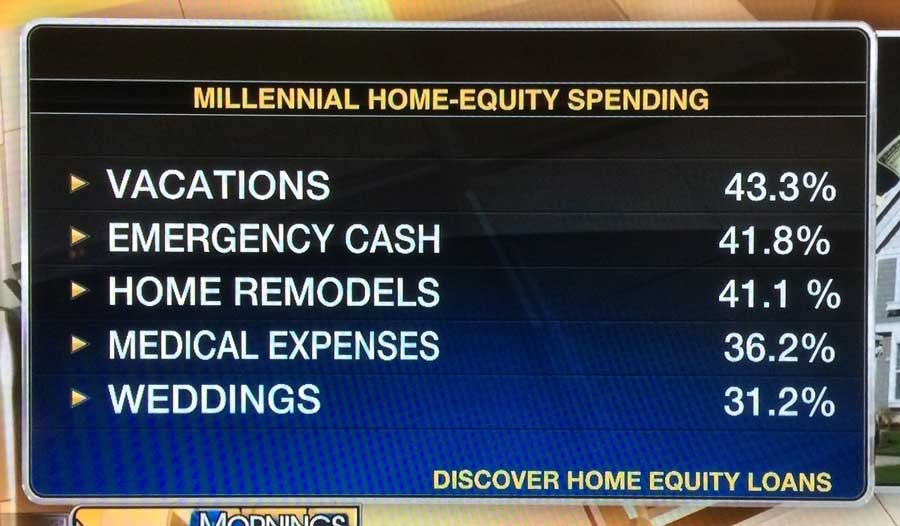

Home values collapsed and delinquencies rose as unemployment grew. Eventually leveraged homeowners couldn’t keep their homes nor pay their debts. We entered the worst recession since the great depression of the 1930s. Now, nearly a decade later, home values are rising again … and both banks and consumers are back at it again. Interestingly the millennial generation (first time home buyers) are following the footsteps of their parents and borrow against their newly acquired homes. But instead of using it as a "home improvement loan" … or even for a larger capital purchase … some focus "experiencing life" or extravagant travel and vacations on credit. The home has now become the low interest credit card!

Some, including Dagen McDowell of Fox Business, argued that this is responsible money management and cheaper than putting it on a credit card. Others … the rest on the Mornings with Maria panel (above photo) … viewed it as "dangerous, irresponsible and the sort of borrowing that brought on the last housing crisis and recession." I chuckled when they began the "get off my lawn" jokes because it was "déjà vu all over again." It brought back memories of boomers being chastised by their parents for extending mortgages longer than 20 years or heaven forbid, borrowing more for home improvements rather than swiftly getting out of debt … let alone using the equity to pay for college or something as frivolous as wedding (cough, cough — guilty).

A clip that I thought was interesting was the discussion on a previous day about living within ones means … don’t spend more that you have and that it is important to save for retirement. Hard hitting (not unlike Dave Ramsey and his "rice and beans, beans and rice advice,") but critically important to be planning long term. Larry Winget was right, there are 40 years to save for retirement, but it all starts with living a lifestyle your income can afford — good advice for Washington DC too.

The latest Intel Optane data storage may be the next big advance for servers and PCs if this is the next chip technology. I’m not sure about power requirements, but perhaps it will make its way in to mobile devices?

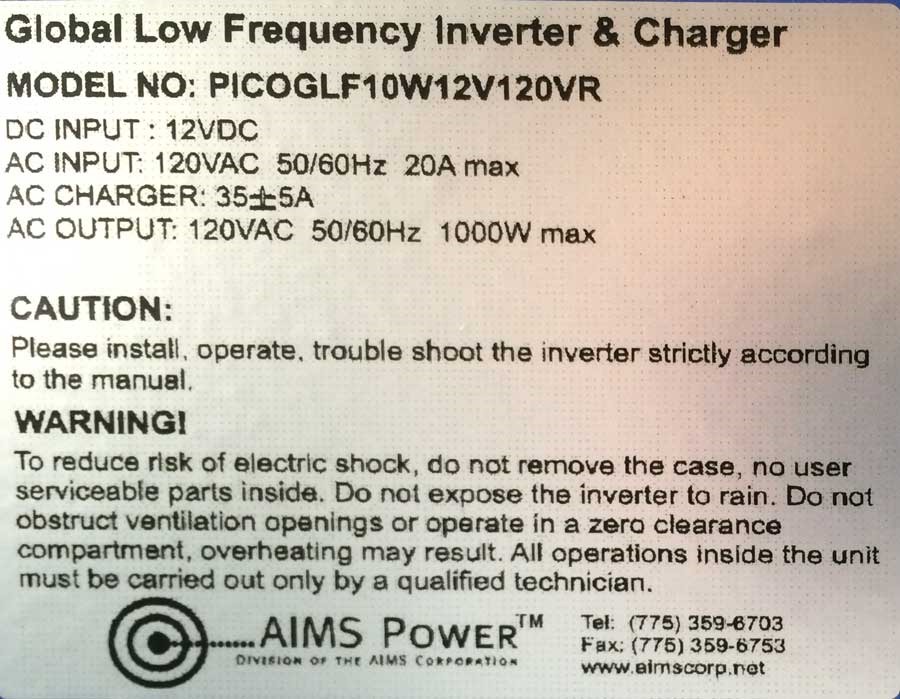

After we “cooked” our generator (my fault for not telling Brenda to prop open the enclosure door), I’ve been tinkering to get parts in order to fix it as mentioned before … but my best attempt as scrounging parts has failed. I could only come up with a possible match for the windings and the price was that of a new generator!

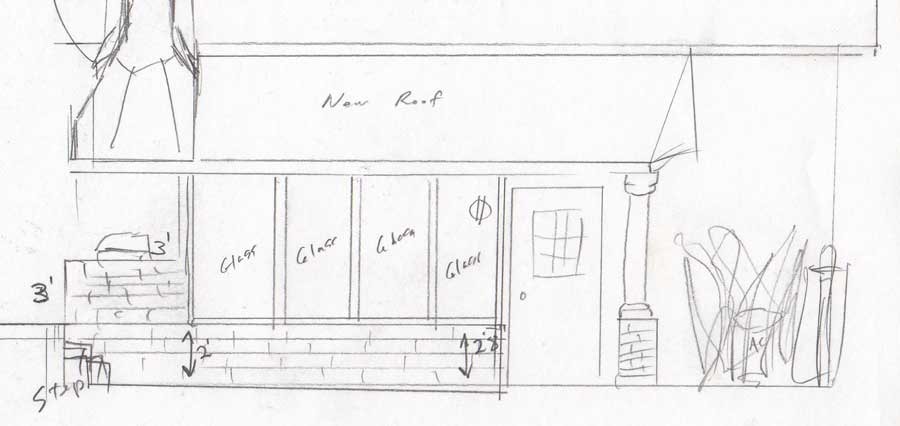

So … when I spotted a small “quieter” Predator inverter-style compact generator on sale at a third of the price of the superb Honda EU2000i that we use on the boat … yet can produce a few more watts (2200 watts plus surge of 2500 watts), I bought it. I’m reworking my entire back-up power plan and have decided to tie in a couple of solar panels, deep cycle batteries and an inverter along with this generator when I build out my grill/greenhouse/rain porch idea (including a photo of the rain flashing above as a concept of bending stainless steel to prevent water from getting behind the stone veneer just as we did for our chimney repair last year).

After removing the old generator and plastic storage box that stood on the sidewalk pad, this new smaller generator should greatly improve the space I have to work with, particularly if I include it inside the greenhouse space. I experimented by wiring a special 20 amp to 30 amp pigtail to test the current 6 circuits use with the old 5000 watt Generac and was shocked at how well this new Predator did in my 3 hour break-in test (burned less than 1/2 gallon of fuel). All six circuit remained powered including kitchen lights and our new refrigerator, furnace fan (no AC obviously), the master bedroom, high draw Plasma TV and my entire home office setup. The biggest drain was when the sump pump kicked in which could be a problem IF other big draw items are on. Realistically though, 95% of the time I can monitor what we use.

As a side note, the above 4 prong 30 amp receptacle is expensive! I shopped it as best I could and still ended up spending $20 plus 2 new 20 amp 110 volt plugs only to realized that one of the cans of spares my dad had collected (and that I brought home from Sidney) was full of plugs that I could have used (no 4 prong 30 amp though!). I realized that I have too much unorganized junk.

Now all I need to do is negotiate with Brenda (previously mentioned kitchen project) in order to fund my grill/greenhouse/generator outside space!

The weekly "My Ride" article by A. J. Baime in the Wall Street Journal has become a sentimental favorite column as besides highlighting a Mercedes a couple weeks ago, did the same for a Packard this week. The story plots are almost always as unique as the cars themselves … although this one touches a sentimental spot with me (not that I have room, but do like this 1956 Packard Executive – fewer than 3000 were made before closing the Detroit factory in the weaning days of Packard). I think for most automotive enthusiasts, the demise of such a treasured American company and brand, as well as many other, were dark days for car-lovers — "Not since the 1930s had so many makes disappeared: Packard, Edsel, Hudson, Nash, DeSoto, and Kaiser."

A military veteran explains why she splurged on a 1956 car that represents the end of an automotive era.

When you’re serving overseas in the military, you meet a lot of people who say, “When I get home, I’m going to do X, Y, and Z.” A lot of times, cars come up in those conversations. Service persons, when they’re deployed, often dream of being at home in a vehicle they would love to have.

I served in Iraq from 2004 to 2007, and when I got home, I didn’t splurge. I did things I thought were practical. But I always dreamed of owning a classic car, and I’m surrounded by beautiful cars every day where I work. [The Malcolm Pray Achievement Center uses a collection of classic cars to teach students about entrepreneurialism.] Last year, I decided the time was right. I was getting married to my now-husband, Irwin Medina, and I wanted a special car for that special day.

Just another ingenious Indiegogo project attempting to raise capital through crowdfunding. We probably don’t need them in the states, but it would be a great option for Minneapolis bike riding … just thinking about my daughter and son-in-law!